Over the weekend, Alan Blinder in the New York Times and Ambrose Evans-Pritchard in the Telegraph both noted that that the real threat currently facing the U.S. economy is not inflation but deflation. One only needs to look at the large negative output gap, the dramatic collapse in nominal spending, or the declines in velocity and the money multiplier to see that there is merit to their claims. There is a real deflationary threat lingering over the U.S. economy in 2009.

With that said, there is an unfortunate irony to the current deflationary threat that can be traced back to 2003. Back then there was another deflationary threat that concerned the Federal Reserve (Fed). As a result, the Fed lowered the federal funds rate to what was at the time an historically low value of 1%. It held this short-term interest rate there for a year before gradually tightening. As we now know, this excessively-loose monetary policy was an important contributor to the buildup of the economic imbalances that eventually led to this economic crisis, including the current deflationary threat. In short, the fear of deflation in 2003 laid seeds for the deflationary threat of 2009.

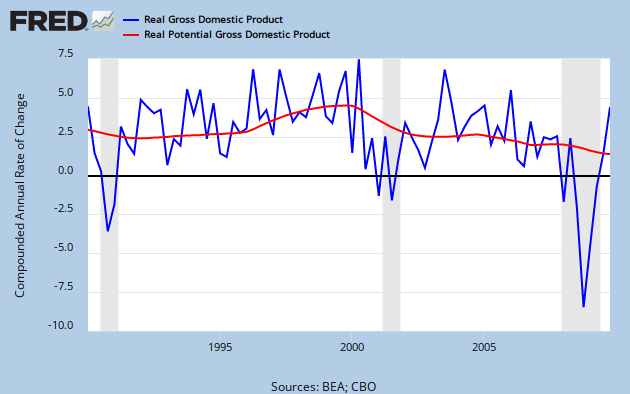

What makes this an unfortunate irony is that this chain of events did not have to happen. For there was a big difference between the deflationary pressures in 2003 and the ones in 2009. In 2003 the deflationary pressures were driven by rapid productivity gains and were benign in nature. Moreover, nominal spending or aggregate demand was rapidly growing. There simply was no evidence of a malign deflationary threat as there is today and thus, there was no need for the Fed to drop interest rates so low for so long. I have documented these developments in previous posts, but here are a few key graphs that make the case. First, here is the year-on-year productivity growth rate plotted against the ex-post real federal funds rate (click on figure to enlarge):

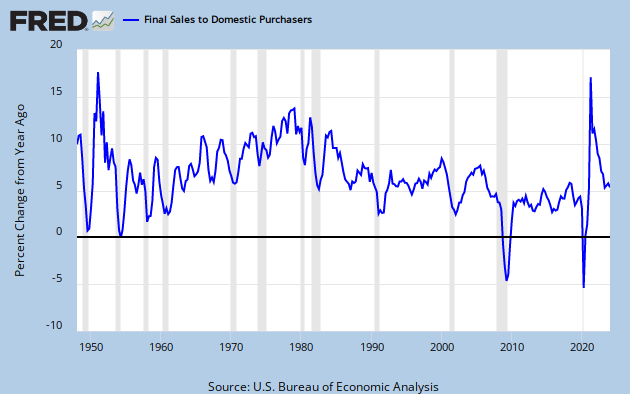

This pictures shows that Fed was pushing the real federal funds rate into negative territory just as productivity was increasing. The next figure shows final sales to domestic purchasers, a measure of nominal spending in the United States plotted against the federal funds rate. The year 2003 is marked off by the dotted lines (click on figure to enlarge):

No indication here of a collapse in nominal spending in 2003. (There was the weak labor market in 2003, but as I have argued before the slow recovery of employment can most likely be traced to (1) the robust productivity gains and (2) the inordinate substitution of capital for labor given the low interest rates of the time.) What this all means is that the Fed's misreading of the deflationary pressures in 2003 contributed to the creation of deflationary pressures of 2009.

My hope is is that moving forward the Fed and other monetary authorities will be more careful in assessing the sources of and responding to the deflationary pressures.

{kind=link}

{kind=link}

With that said, there is an unfortunate irony to the current deflationary threat that can be traced back to 2003. Back then there was another deflationary threat that concerned the Federal Reserve (Fed). As a result, the Fed lowered the federal funds rate to what was at the time an historically low value of 1%. It held this short-term interest rate there for a year before gradually tightening. As we now know, this excessively-loose monetary policy was an important contributor to the buildup of the economic imbalances that eventually led to this economic crisis, including the current deflationary threat. In short, the fear of deflation in 2003 laid seeds for the deflationary threat of 2009.

What makes this an unfortunate irony is that this chain of events did not have to happen. For there was a big difference between the deflationary pressures in 2003 and the ones in 2009. In 2003 the deflationary pressures were driven by rapid productivity gains and were benign in nature. Moreover, nominal spending or aggregate demand was rapidly growing. There simply was no evidence of a malign deflationary threat as there is today and thus, there was no need for the Fed to drop interest rates so low for so long. I have documented these developments in previous posts, but here are a few key graphs that make the case. First, here is the year-on-year productivity growth rate plotted against the ex-post real federal funds rate (click on figure to enlarge):

This pictures shows that Fed was pushing the real federal funds rate into negative territory just as productivity was increasing. The next figure shows final sales to domestic purchasers, a measure of nominal spending in the United States plotted against the federal funds rate. The year 2003 is marked off by the dotted lines (click on figure to enlarge):

No indication here of a collapse in nominal spending in 2003. (There was the weak labor market in 2003, but as I have argued before the slow recovery of employment can most likely be traced to (1) the robust productivity gains and (2) the inordinate substitution of capital for labor given the low interest rates of the time.) What this all means is that the Fed's misreading of the deflationary pressures in 2003 contributed to the creation of deflationary pressures of 2009.

My hope is is that moving forward the Fed and other monetary authorities will be more careful in assessing the sources of and responding to the deflationary pressures.

On a technical note, the output gap may not be as great as that graph shows. According to the San Francisco Fed, it may only be -2%!!

ReplyDeleteSee http://blogs.wsj.com/economics/2009/06/15/fed-study-raises-doubt-about-economys-slack/

ECB:

ReplyDeleteInteresting...I like that this alternative measure of the output gap actually shows a postive value during the height of the housing boom.

Not being an economist myself, I have nevertheless been wary about the deflation-hysterics which has lately been fuelled by media reports about (slightly) falling prices.

ReplyDeleteWhen one considers [with Prof. …. and others] overheated commodity-prices (in particular crude oil) as one of the driving forces behind our economic calamity, it sounds strange to hear some voices deplore a modest decline in consumer prices, those very same prices which had previously been inflated by the enormous (speculative?) rise in particular of the oil and gas prices and which now go down primarily because that commodity bubble has burst.

To view deflation as an economic problem during the Great Depression seems to make sense. As for Japan’s “Lost Decade”, I’ve always failed to understand how a country’s economy was supposed to be trapped in a vicious cycle of underconsumption through falling consumer prices but still enjoy a (small) growth rate.

Thanks to your blog and Cato-Paper and to some of the other studies that you have linked to, I now feel quite secure that deflation in itself is not the media-depicted bogeyman and that it was in fact an unwarranted deflation-Angst that helped get us into the mess of our financial and economic crises.

While it seems rational and convincing to trace the deflation-fear back to the experiences of the Great Depression, there still might be deeper rooted motives at work, motives that the actors (or at least the great majority of those) are not themselves necessarily aware of.

Could it be that “the financial system” has its very own (egoistic) reasons to prefer inflation over deflation? Wouldn’t it be easier to get people sucked into debt in an inflationary environment rather than in a (mildly) deflationary one?

Now I’m not claiming that the deflation scare is owed to a conspiracy of the media or whoever else. It might be worthwhile though to analyse the interest of the actors in the financial industry (or, as I would prefer to call it, ‘Organized Finance’). If there is reason to believe that objectively they fare better with a little inflation than a little deflation it would make sense to assume they would at least instinctively support an inflation target rather than stable or falling prices.

I lack the education to make an educated guess in detail about possible mechanisms. But on a very general level it would seem that ‘Organized Finance’ would prefer more money over less money floating around. The more there is, the more they can clip off a bit for themselves. Just like in the olden days with gold coins: more coins, more chances for clipping.

Lorenzo Bini Smaghi, Italian Member of the ECB's Executive Board ( http://www.ecb.int/ecb/orga/decisions/html/cvbinismaghi.en.html ), seems to share your view about how Alan Greenspans crusade against deflation in 2003/2004 set the stage for our contemporary economic disaster.

ReplyDeleteIn an article (in German) in the Financial Times (Deutschland) from April 19 under the heading "Deflationsangst. EZB-Notenbanker warnt vor Überreaktion" (Deflation-fear. ECB-Banker warns against overreaction - http://www.ftd.de/finanzen/maerkte/:deflationsangst-ezb-notenbanker-warnt-vor-ueberreaktion/502368.html ) Bini Smaghi is reported to have told the paper (FTD):

"Wir sollten nicht vergessen: Fehler bei der Vorhersage einer Deflation, das heißt der Deflation eine zu große Bedeutung beizumessen, sind zentrale Gründe für die jetzige Krise" ... . 2003 und 2004 seien die Leitzinsen aus "übertriebenen Deflationsängsten" zu stark gesenkt worden.

In (my) English (not overly elegant):

"We should not forget: mistakes in the prognosis of a deflation, i. e. overestimating the importance of deflation, have been central causes for our present crisis".

In 2003 and 2004 the prime rates [he said] have been lowered too much due to "excessive deflation-fears".

If that's not an official recognition of your opinion ... (except that Bini Smaghi does not identify the reasons for the 2003 deflationary tendencies).

[Also interesting to read is B.-S's speech "Careful with (the D) words!" from Nov. 2008 - http://www.bis.org/review/r081127e.pdf?noframes=1 ]

Thanks for the links Cangrande. I trust you have seen William White's work at the BIS. He has a number of great pieces, but I especially liked his paper titled "Is Price Stability Enough?" (http://www.bis.org/publ/work205.pdf)

ReplyDeleteAlso, I would point out George Selgin's "Less the Zero" (http://www.amazon.com/Less-Than-Zero-Falling-Growing/dp/0255364024)

All the best.

David