Brad Delong is wondering whether the Federal Reserves' low interest rate policy in the early-to-mid 2000s was truly a mistake:

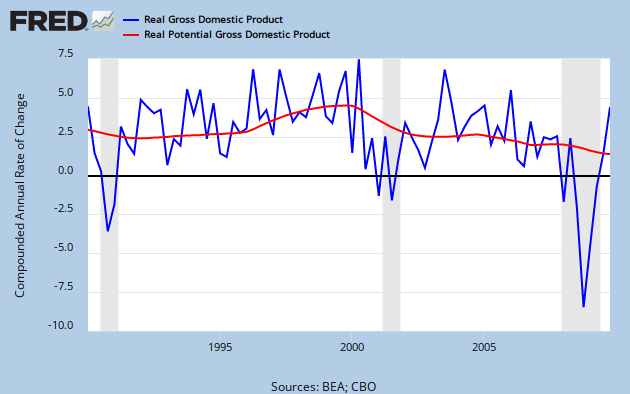

Here we see productivity growth soaring just as the real federal funds rate is being pushed into negative territory. Normally, a rise in productivity growth should lead to a rise in the natural interest rate and ultimately, a rise in the federal funds rate for monetary policy to stay neutral. However, this latter development did not happen. It seems, then, the Fed did push its policy rate below the natural rate and in the process created a huge Wicksellian-type disequilibria. This interpretation of events has been borne out more rigorously in this ECB paper. One a more practical level, this disequilbria comes through in the Taylor rule which similarly shows the federal funds rate was below the neutral rate during this time.

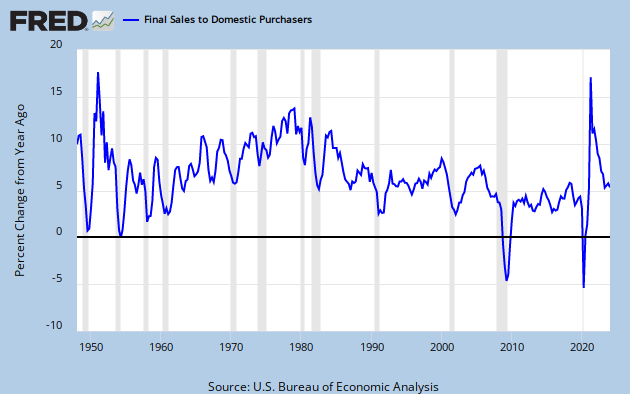

It is also worth noting that these same rapid productivity gains were the source of the deflationary pressures in 2003 that Brad mentions. Thus, these deflationary pressures did not indicate a weakening economy. In fact, aggregated demand (AD) was growing at at rapid rate in 2003-2004 which, if anything, indicated an overheating economy. The figure below shows a measure of AD, final sales to domestic purchasers, relative to the federal funds rate and has the period 2003-2004 marked off by the dotted lines (click on picture to enlarge):

The productivity gains, apparently, were offsetting the upward pressure on prices being created by the robust growth in AD at this time. There simply was no real deflationary threat in 2003. By way of contrast, this figure shows for 2008-2009 what a real AD-induced deflationary threat looks like. Regarding the saving glut theory I would recommend Menzie Chinn's post here or my previous post here.

The final data issue is the weak employment growth coming out of the 2001 recession. Given the above discussion, the best interpretation of this development is there was less demand for labor in the recovery given the productivity gains. In fact, this was common explanation given at the time. One could also argue that the Fed's low interest rate policy may have pushed some firms to inordinately substitute out of labor to capital.

Here is the bottom line: there is enough evidence for Brad DeLong to conclude that Federal Reserve's low interest rate policy was a mistake.

Update: Brad DeLong responds to this and other posts.

There is, however, active debate over whether there was a fourth mistake: whether Alan Greenspan's decision in 2001-2004 to push and keep nominal interest rates on Treasury securities very very low in order to try to keep the economy near full employment was a fourth mistake...I am genuinely not sure which side I come down on in this debate.Brad's uncertainty is understandable given he invokes the entire 2001-2004 time frame. For during this period there was a time when the U.S. economic recovery was sputtering along (2001-2002) and a time when the recovery began to take hold (2003-2004). It was during this latter period that Fed's low interest rates were a big mistake. But even for that period I think Brad is misreading the data:

People claim that the Greenspan Federal Reserve "aggressively pushed the interest rate below its natural level."... [T]he market interest rate[, however,] was if anything above the natural interest rate in the early 2000s: not accelerating inflation but rather deflation threatened. The natural interest rate was very low because, as Ben Bernanke explained at the time, the world had a global savings glut (or, rather, a global investment deficiency). You can argue--and on Tuesdays and Thursdays I will believe you--that Alan Greenspan's policies in the early 2000s were wrong. But you cannot argue that he aggressively pushed the interest rate below its natural level. The low interest rate was at its natural level.I think the evidence shows the opposite. The natural interest rate is a function of individual's time preferences, productivity, and the population growth rate. Of these three components, the one that changed the most in 2003-2004 was productivity as can be seen in the figure below (click on figure to enlarge):

Here we see productivity growth soaring just as the real federal funds rate is being pushed into negative territory. Normally, a rise in productivity growth should lead to a rise in the natural interest rate and ultimately, a rise in the federal funds rate for monetary policy to stay neutral. However, this latter development did not happen. It seems, then, the Fed did push its policy rate below the natural rate and in the process created a huge Wicksellian-type disequilibria. This interpretation of events has been borne out more rigorously in this ECB paper. One a more practical level, this disequilbria comes through in the Taylor rule which similarly shows the federal funds rate was below the neutral rate during this time.

It is also worth noting that these same rapid productivity gains were the source of the deflationary pressures in 2003 that Brad mentions. Thus, these deflationary pressures did not indicate a weakening economy. In fact, aggregated demand (AD) was growing at at rapid rate in 2003-2004 which, if anything, indicated an overheating economy. The figure below shows a measure of AD, final sales to domestic purchasers, relative to the federal funds rate and has the period 2003-2004 marked off by the dotted lines (click on picture to enlarge):

The productivity gains, apparently, were offsetting the upward pressure on prices being created by the robust growth in AD at this time. There simply was no real deflationary threat in 2003. By way of contrast, this figure shows for 2008-2009 what a real AD-induced deflationary threat looks like. Regarding the saving glut theory I would recommend Menzie Chinn's post here or my previous post here.

The final data issue is the weak employment growth coming out of the 2001 recession. Given the above discussion, the best interpretation of this development is there was less demand for labor in the recovery given the productivity gains. In fact, this was common explanation given at the time. One could also argue that the Fed's low interest rate policy may have pushed some firms to inordinately substitute out of labor to capital.

Here is the bottom line: there is enough evidence for Brad DeLong to conclude that Federal Reserve's low interest rate policy was a mistake.

Update: Brad DeLong responds to this and other posts.

{kind=link}

{kind=link}

{kind=link}