(1) James Hamilton gives us a reality check on the U.S. debt-to-GDP ratio. He shows that we should not take comfort, as some observers do, in comparing the current value of this ratio to what is was coming out of WWII. Back then there was far more non-mandatory spending that could easily be pared down. A very sobering read. [Update: Paul Krugman replies to Hamilton]

(2) David Andolfatto meanwhile is more optimistic on the growing U.S. debt-to-GDP ratio. He cites Ricardo Caballero's argument that there is a shortage of high-quality financial assets in the world and thus the large increase in U.S. Treasuries is actually an optimal outcome. The world needs our Treasuries and the only way we can provide them is to incur more public debt.

(3) Menzie Chinn has a new paper with Jeffry Frieden where they look at the causes and consequences of the current economic crisis. Among other things, they note that the excess savings from the rest of the world was not forced on the United States. Rather, it responded to the excess U.S. demand pressures created by loose fiscal and monetary policies in the United States. They put more emphasis on fiscal policy than I would, but their key point that U.S. economic policies were the important drivers in the buildup of global economic imbalances is spot on.

(4) Tyler Cowen does a Milton Friedman smackdown of David Henderson. Tyler shows, contrary to David's claims, that Milton Friedman thought the Fed in 1929-1931 period should have (1) bought up a lot more bonds (i.e. increased the money supply) and (2) acted a lender of last resort (i.e. done more to prevent the banking system collapse). In short, Milton Friedman was for both stabilizing the money supply and bailing out the banking system. As Tyler notes, the idea of bailouts is hard for many libertarians to swallow, but the alternative may be a far worse outcome for them.

(5) Speaking of running, Justin Wolfers reminds us there is an opportunity cost to this sport. However, he does the calculations and concludes that training for a marathon is an optimal outcome for him.

Macro Musings Blog

Friday, August 28, 2009

Assorted Musings

Some assorted musings:

Wednesday, August 26, 2009

Critically Assessing Bernanke's Record

Now that Bernanke has been renominated to lead U.S. monetary policy his time at the Fed is being critically assessed by a number of observers. Here are five assessments:

(1) Simon Johnson says there are multiple versions of Bernanke--the one that saved the financial system after the Lehman-AIG collapse, the one that intellectually justified Greenspan's low interest rate policy and indifference to asset bubbles, and the one that has pushed for reform of the financial system--and would like to know which one we are going to get in his second term. He also is resigned to the fact that the current Fed policies will most likely lead to another bubble and financial crash.

(2) Stephen Roach highlights three critical mistakes Bernanke made: (i) he saw no need for the Fed to preempt asset bubbles, (ii) he was the intellectual architect of the saving glut view that allowed the Fed to turn the other way when housing boom was taking off, and (iii) he failed to take seriously the need to get a handle on the seriousness of the derivative explosion, the shadow banking system, and the extent of leverage in the U.S. economy.

(3) Ambrose Evans-Pritchard notes that it was Bernanke who provided "academic cover" for (i) Greenspan's view that asset bubbles do not matter and for (ii) holding down interest rates for so long below their neutral level.

(4) Desmond Lachman believes Bernanke's heroic efforts over the past nine months must not overshadow the indifference Bernanke's Fed had toward the housing boom in 2006 and 2007 leading up to the crisis nor his role in the Lehman debacle.

(5) Barry Ritholtz acknowledges that Bernanke's endorsement of Greenspan's interest rate policies were problematic and that his views on asset bubbles and the saving glut gave credence to the Fed's indifference to the housing boom. However, Ritholtz ultimately holds Greenspan accountable for the policies of that time.

Tuesday, August 25, 2009

The Future of U.S. Monetary Policy

Stephen Roach is not pleased with Obama's nomination of Ben Bernanke as the next Fed chair. Despite this outcome, Roach is hopeful that this decision will create a national debate on what should be the objectives U.S. monetary policy going forward:

The Bernanke reappointment is a welcome chance for a broader debate over the conduct and role of US monetary policy. Mr Obama has made sweeping proposals that give the Fed broad new powers in managing systemic risks. I argued in the Financial Times 10 months ago that the Fed should not be granted these powers without greater accountability as required by a “financial stability mandate” – in effect, forcing the Fed to shape monetary policy with an aim towards avoiding asset bubbles and imbalances. Without a revamped policy mandate, it is conceivable that we could face another destabilising crisis.I hate to sound like a broken record, but a nominal income targeting rule would go a long way in improving financial stability.

Is Deflation Still a Threat?

Reuter's Christopher Swann says yes. He explains the nature of the current deflationary pressures and argues they still pose a threat:

One thing I like about Swann is that he takes the time to explain why today's deflationary pressures are harmful--they are driven by a collapse in aggregate demand--and different than the more benign deflationary pressures that occurred earlier in the decade--they were driven by an increase in aggregate supply. This is the view I hold as noted here and here. Finally, note that the fundamental problem here is not deflation per say but a collapse in nominal spending. That is why we need more than ever a nominal income targeting rule.

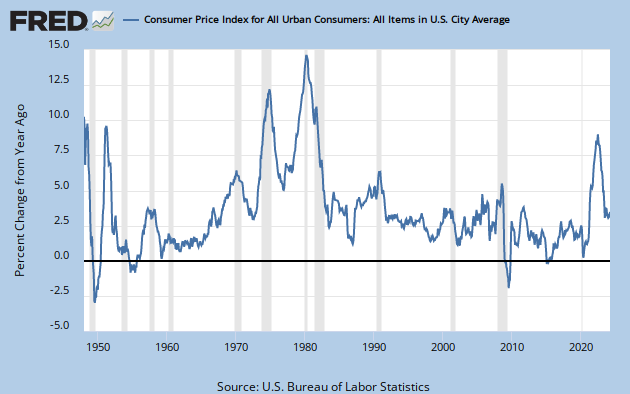

Swann cites research in the piece that core inflation is overstated by 1%. Headline CPI inflation on a year-on-year basis has been negative as can be seen in this graph. TIPs securities, however, show an expected average rate of inflation over the next 5 years that is positive at about 1.3%.The current variety of deflationary pressure... stems not from efficiency savings but rather from weak demand. Worse still, it is accompanied by record levels of debt.

Despite frantic efforts to pay off loans, household debt is still around 130 percent of disposable income. This was precisely the combination that Irving Fisher warned about in his celebrated 1933 article on debt deflation.

Under these conditions, the rising real value of debts encourages households and businesses to sell their assets to pay down loans. As fire sales reduce asset prices — stocks and property — real net worth declines further. Output and employment decline, accelerating the slide in prices.

[...]

So we are right to be afraid of deflation — very afraid. It still has the potential to sap energy from the American economy for years to come.The Federal Reserve is preparing to lay down its unorthodox monetary policy instruments. But it may have to dig deep into its tool box before too long if deflation takes hold.

One thing I like about Swann is that he takes the time to explain why today's deflationary pressures are harmful--they are driven by a collapse in aggregate demand--and different than the more benign deflationary pressures that occurred earlier in the decade--they were driven by an increase in aggregate supply. This is the view I hold as noted here and here. Finally, note that the fundamental problem here is not deflation per say but a collapse in nominal spending. That is why we need more than ever a nominal income targeting rule.

Monday, August 24, 2009

Dark Clouds on the Horizon?

Nouriel Roubini says there may be trouble ahead:

There are also now two reasons why there is a rising risk of a double-dip W-shaped recession. For a start, there are risks associated with exit strategies from the massive monetary and fiscal easing: policymakers are damned if they do and damned if they don’t. If they take large fiscal deficits seriously and raise taxes, cut spending and mop up excess liquidity soon, they would undermine recovery and tip the economy back into stag-deflation (recession and deflation).If that were not enough, Andy Xie shares a similar outlook.

But if they maintain large budget deficits, bond market vigilantes will punish policymakers. Then, inflationary expectations will increase, long-term government bond yields would rise and borrowing rates will go up sharply, leading to stagflation.

Another reason to fear a double-dip recession is that oil, energy and food prices are now rising faster than economic fundamentals warrant, and could be driven higher by excessive liquidity chasing assets and by speculative demand. Last year, oil at $145 a barrel was a tipping point for the global economy, as it created negative terms of trade and a disposable income shock for oil importing economies. The global economy could not withstand another contractionary shock if similar speculation drives oil rapidly towards $100 a barrel.

An Inspiring Picture

This is off topic, but I find this picture inspiring (click on figure to enlarge):

It is a picture of the Antarctica Marathon. Here is a description of the event:

It is a picture of the Antarctica Marathon. Here is a description of the event:

The 11th Antarctica Marathon & Half-Marathon is scheduled for March 7, 2010. You will come face to face with icebergs, penguins, seals and whales while exploring the most pristine corner of the planet. Historians and scientists will provide lectures on board ship and wildlife excursions during landings in remote areas among seal colonies and penguin rookeries and at research bases.I find these exotic marathons alluring and would one day love to do one or more. In addition to the Antarctica Marathon there is the Great Wall Marathon and Mt. Kilimanjaro Marathon, among others. For now I will settle for the Houston Marathon and feel good about warding off lung and gastrointestinal cancer.

Get Ready for Interest Rate Shocks

One of the important messages coming out of the central banker's annual retreat in Jackson Hole, Wyoming is that once the crisis is over the Federal Reserve's (Fed) tightening of monetary policy may be abrupt. If so, increases in short term interest rates will not be gradual but jarring. The reasoning behind this approach, as I understand it, is that (1) since there could be political pressures to monetize the government debt and (2) given the large amount of existing liquidity that needs to be drained the Fed's exit strategy needs to be unmistakably clear in communicating that it will not tolerate the unanchoring of inflationary expectations. Here is the New York Times:

A growing number of economists and some Fed officials say the shift to tighter monetary policies and higher interest rates, though unlikely to start until at least the middle of next year, may have to be much more abrupt than normal if they are to prevent inflation two or three years from now.And here is the Wall Street Journal on the talk Carl Walsh gave at the retreat:

“When you get into a crisis like this, gradualism is not the right strategy,” said Frederic S. Mishkin, an economist at Columbia University who was a Fed governor from 2006 until 2008. “Of course, when things turn around, you have to be aggressive in the other direction.”

[O]nce the Fed does start raising the federal-funds rate out of its current record-low range near zero, "it should be increased quickly," Mr. Walsh argued. "There is no support for raising rates at a gradual pace once the zero rate policy is ended."This rhetoric is sounding so Paul Volker-like. It remains to be seen, though, whether the Fed could actually make such abrupt changes in monetary policy. There are two major obstacles to such an approach. First, now that the global economy has become addicted to a low interest rate policy, any drastic tightening will amount to a painful interest rate shock. Second, tightening policy may make the budget deficits even larger and make it more costly to finance, a point alluded to in the New York Times article:

Indeed, the Federal Reserve’s “exit strategy” could lead to a clash with the Obama administration. The White House plans to release its newest budget estimates next week, and administration officials said that the 10-year deficit will rise to $9 trillion — a big jump from its earlier estimate of $7 trillion.

[...]

In the future, Fed officials could feel more pressure to further tighten monetary policy as a way of countering the government’s deficit spending. The immense amount of borrowing could push up long-term interest rates, if foreign investors balk at buying up United States debt.

Of course, all of this analysis assumes the Fed knows when the time is right to begin its exit strategy. As noted in my previous post, however, even this assumption is questionable. Fed policy over the next few years should be a doozy to watch.

Thursday, August 20, 2009

A Big Challenge for the Fed

David Altig recently recently considered the question of how fast the U.S. economy could recover from the recession. He noted that in order to answer this question one would need to know how much spare capacity there is in the U.S. economy. A lot of excess capacity means there are underutilized resources that can easily be employed without straining the economy--a rapid recovery is possible. However, if there is little or no spare capacity then the opposite is true. The standard measure of excess capacity in macroeconomics is the output gap: the difference between actual and potential GDP. A positive output gap means the economy is growing too fast; a negative value indicates there is excess capacity.

So what is the current output gap? As David Altig notes, no one knows for sure and there is wide variation among the current estimates:

Update: Arnold Kling has a few things to say about the output gap.

So what is the current output gap? As David Altig notes, no one knows for sure and there is wide variation among the current estimates:

To wit, there is substantial variation in output gap estimates across the different methods, and I do mean substantial: The gap estimates for the second quarter of 2009 range from –0.5 to nearly –11 percent depending on which method is used. In other words, some methods imply the gap is very large, others say the gap is rather small.Now this output gap uncertainty presents problems not only for forecasting how fast the U.S. economy will recover, but also for the Fed's exit strategy. For the Fed to correctly time its exit strategy it needs to know the output gap. Otherwise, it could risk repeating the 1970s inflation debacle. This point was articulated by Edward Chancellor recently in the Financial Times:

[T]he Fed will likely remain passive until the economy is running near full capacity, or what economists call the “output gap” has narrowed. This sounds sensible. After all, inflation comes about when too much money chases too few goods and services, causing the economy to overheat.The trouble is that the track record of economists measuring the output gap in real time is rather patchy, to say the least.I would note that one of the assumptions in the above discussions is that the Fed aims to stabilize inflation. Given this objective, getting the estimate of the output gap right correct is a big deal for the Fed. Of course, if the Fed were to move to a nominal income targeting rule then the output gap issue would be moot. Just another reason to rethink nominal income targeting.

Research by Athanasios Orphanides, a former Fed staffer and the current head of the Cypriot central bank, reveals the limitations of output gap analysis. This gap is said to exist when current output is below its trend level. Unfortunately, economists can’t agree on which statistical techniques best measure this trend. Different methods produce widely differing estimates of the output gap; they even differ as to whether the sign is positive or negative. For instance, at the turn of the century the European Central Bank reckoned the output gap for the eurozone to be negative (ie potentially inflationary). In later years this figure was revised as positive. Subsequent revisions to the output gap have been as large as the original estimate.

Historically, the greatest errors in the measurement of the output gap have occurred at times when the economy entered a period of structural change. In late 1973, for example, businesses were forced to adapt to a sudden threefold rise in the price of oil. During the recession which followed, contemporary calculations suggested the US economy was operating at around 10 per cent below capacity. Only later did it become clear that the energy crisis constituted a “supply shock”, rendering much embedded capacity redundant and shifting the economy to a lower trend growth rate.

At the time, the Federal Reserve failed to recognise the impact of this supply shock. In response to what was then believed to be a mere cyclical downturn, interest rates were kept low. Only subsequently was it revealed that the economy was operating at near full capacity despite large unemployment and that monetary policy was too loose. By then it was too late to prevent the great stagflation.

Update: Arnold Kling has a few things to say about the output gap.

Wednesday, August 19, 2009

The Economics of Sex and Drug Use

Scott Cunningham is friend of mine from graduate school. Unlike me, he was wise enough to steer away from macroeconomics and instead got hooked on labor and health economics. Within this field he has done a lot of interesting work on the economics of sex and drug use. Here are some of his studies:

“Using Political Conventions to Estimate the Responsiveness of Prostitution Labor Supply” (with Todd Kendall)Abstract: In late August and early September, 2008, approximately 100,000 visitors came to Denver, Colorado and Minneapolis, Minnesota to attend the Democratic and Republican National Conventions. Economic theory suggests that males in transit can cause a shift in demand for commercial sex work. We estimate the responsiveness of labor supply to these two conventions, focusing on a previously neglected but increasingly important segment of the prostitution market: professional escorts who advertise on local prostitution solicitation websites. We find that the conventions caused a 35%-195% increase in advertisements in the affected markets.“Prostitution, Technology and the Law: New Data and Directions” (with Todd Kendall)

Abstract:The phenomenon of prostitution is an important determinant for marriage, divorce, intra‐family bargaining power, and polygamous activity, and has been a touchstone of government regulation. Recently, new communications technologies have changed the industrial organization of prostitution suppliers, potentially expanding this underground market in developed countries. We describe the institutions of prostitution as they exist in developed countries and how technology has affected these institutions. We describe several databases researchers can employ to study modern prostitution and we illustrate the value of these data with several empirical analyses, including a hedonic evaluation of prostitute characteristics and services, an analysis of the effects of an important change in the regulation of prostitute advertisement, and an estimate of the marital and family characteristics of technology‐facilitated prostitutes.

“Parental Methamphetamine Use and Foster Care: Is the Growth in Foster Care Admissions Explained by the Growth in Meth Use?” (with Greg Rafert)

Abstract: Although foster care caseloads have almost doubled over the last two decades, little is known regarding the factors that contributed to this significant growth. This article focuses on one factor, parental illicit drug use, and examines the relationship between parental drug use and foster care admissions. To mitigate the impact of omitted variable and simultaneity bias, we take advantage of two significant, exogenous supply-side interventions in the methamphetamine market, and find robust evidence that methamphetamine use has led in part to the growth in foster care caseloads. Further, in identifying the precise mechanisms that translated growth in methamphetamine use to the observed increase in foster care caseloads, we find that parental incarceration and child neglect have played significant roles in bringing children into the U.S. foster care system. These results suggest that child welfare policies should be designed specifically for the children of methamphetamine-using parents.

“Sex Ratios and Risky Sexual Behavior” (with Christopher Cornwell)

Abstract: Black Americans have dramatically higher rates of sexually transmitted diseases (STD), including HIV/AIDS, despite constituting a mere 12 percent of the population. Epidemiologists have suggested that these racial disparities persist because of a greater degree of concurrency in Black sexual networks, but this invites a question: why is the degree of concurrency higher in Black sexual networks? In this paper, we emphasize the relative shortage of men in Black communities, created largely by the high rates of Black male incarceration. We hypothesize that these high “sex ratios” allow for men with tastes for promiscuity to form concurrent partnerships, as well as affects their condom use.

How Bad Was Hyperinflation in Zimbabwe?

There is an interesting article in the latest issue of the Cato Journal by Steve Hanke and Alex Kwok. In this article, the authors estimate the amount of hyperinflation in Zimbabwe in 2008. This may seem like a trivial task, but no so for Zimbabwe:

In plain English, the monthly rate of hyperinflation was 79.6 billion % in November 2008. That is an astonishing figure. Fortunately, the hyperinflation ended earlier this year when the government shut down its currency-printing presses and allowed foreign exchange to legally circulate. There was, however, a high price to pay for this hyperinflation and there is still much reform needed in Zimbabwe. Here is an excerpt from the IMF's 2009 Article IV for Zimbabwe:

I hope this is truly a new beginning for Zimbabwe.

Even though the Reserve Bank of Zimbabwe produced an ever increasing torrent of money, and with it ever more inflation, it was unable, or unwilling, to report any meaningful economic data during most of 2008. Indeed, the last Reserve Bank balance sheet and money supply data produced in 2008 were for March. As for the 2008 inflation data, the last available figures were for July, and these were not released until October. This data void hid Zimbabwe’s hyperinflation experience under a shroud of secrecy.Hanke and Kwok fills this data void with their hyperinflation estimates. Here is their summary table from the article (click on figure to enlarge):

In plain English, the monthly rate of hyperinflation was 79.6 billion % in November 2008. That is an astonishing figure. Fortunately, the hyperinflation ended earlier this year when the government shut down its currency-printing presses and allowed foreign exchange to legally circulate. There was, however, a high price to pay for this hyperinflation and there is still much reform needed in Zimbabwe. Here is an excerpt from the IMF's 2009 Article IV for Zimbabwe:

Background. The economic and humanitarian situation worsened dramatically in 2008. Hyperinflation, fueled by the RBZ’s quasi-fiscal activities, and a further significant deterioration in the business climate contributed to an estimated 14 percent fall in real GDP in 2008, on top of a 40 percent cumulative decline during the period of 2000–07. Unemployment, poverty, malnutrition, and incidence of infectious diseases have risen sharply.

The official adoption of hard currencies for transactions in early 2009 recognized the de facto virtually complete dollarization of Zimbabwe’s economy. The government also recently announced that the rand would be the reference currency. Dollarization has helped stabilize prices, improve revenue performance, and impose fiscal discipline, including on the RBZ.

Outlook. Reversing output decline and improving social conditions would require determined efforts to maintain sound macroeconomic policies, and to attract domestic and foreign investors and significant donor support. In the absence of cash budget support, higher humanitarian assistance, and wage restraint, the economic and social situation could deteriorate significantly in 2009. Zimbabwe’s external debt burden is unsustainable even if policies are improved and medium-term financing gaps are filled by concessional financing.

Monday, August 17, 2009

Hope and Concern for the Global Economy

This Economist's article gives us hope that Asia may pull the global economy out of its slump:

IT NEVER pays to underestimate the bounciness of Asia’s emerging economies. After the region’s financial crisis of 1997-98, and again after the dotcom bust in 2001, outsiders predicted a lengthy period on the floor—only for the tigers to spring back rapidly. Earlier this year it was argued that such export-dependent economies could not revive until customers in the rich world did. The West still looks weak, with many economies contracting in the second quarter, and even if America begins to grow in the second half of this year, consumer spending looks sickly. Yet Asian economies, increasingly decoupled from Western shopping habits, are growing fast.The article goes on to say the most important part of the Asian recovery is an increase in domestic spending. I hope this Asian spending surge is sustainable because it is needed to offset what Ambrose Evans-Pritchard says is an alarming amount of excess capacity in the global economy:

The four emerging Asian economies which have reported GDP figures for the second quarter (China, Indonesia, South Korea and Singapore) grew by an average annualised rate of more than 10% (see article). Even richer and more sluggish Japan, which cannot match that figure, seems to be recovering faster than its Western peers. But emerging Asia should grow by more than 5% this year—at a time when the old G7 could contract by 3.5%.

Too many steel mills have been built, too many plants making cars, computer chips or solar panels, too many ships, too many houses. They have outstripped the spending power of those supposed to buy the products. This is more or less what happened in the 1920s when electrification and Ford’s assembly line methods lifted output faster than wages. It is a key reason why the Slump proved so intractable, though debt then was far lower than today.Nouriel Roubini provides further words of caution about the recovery of the global economy.

Thankfully, leaders in the US and Europe have this time prevented an implosion of the money supply and domino bank failures. But they have not resolved the elemental causes of our (misnamed) Credit Crisis; nor can they.

Excess plant will hang over us like an oppressive fog until cleared by liquidation, or incomes slowly catch up, or both. Until this occurs, we risk lurching from one false dawn to another, endlessly disappointed.

Justin Lin, the World Bank’s chief economist, warned last month that half-empty factories risk setting off a “deflationary spiral”. We are moving into a phase where the “real economy crisis” bites deeper – meaning mass lay-offs and drastic falls in investment as firms retrench. “Unless we deal with excess capacity, it will wreak havoc on all countries,” he said.

Mr Lin said capacity use had fallen to 72pc in Germany, 69pc in the US, 65pc in Japan, and near 50pc in some poorer countries. These are post-War lows. Fresh data from the Federal Reserve is actually worse. Capacity use in US manufacturing fell to 65.4pc in July.

Friday, August 14, 2009

Fed Smackdown Edition

My critiques of Fed policies in the early-to-mid 2000s are beginning to look tame compared to these observers. First, here is a Free Exchange summary of a Lutz Kilian paper:

[E]xcessively accommodative monetary policy and regulatory policy over the last decade may have led to unsustainably high global growth, which in turn was responsible for a demand driven spike in oil prices. There are two angles to this. One is that the natural unemployment rate was higher than the Fed thought, and the only way to push unemployment below that level was to facilitate bubbles in the financial and housing sectors, which excessively juiced demand and enabled the oil spike. The other is that lax monetary policy kept American consumption at too-high levels, leading to very rapid emerging market growth (which was exacerbated by the fact that dollar pegs led to importation of loose American monetary policy in trading partner economies).Next up is Daniel Gross, Jacopo Carmassi, and Stefano Micossi. They write in this Vox article that too many observers confuse the symptoms of the economic imbalances as causes. For example, they note the following:

Boiling this down, Mr Kilian seems to be suggesting that a monetary policymaker with this reading of the economy would have acted more cautiously than someone with Ben Bernanke's view ("that the oil price shocks of the 1970s and 1980s arose exogenously with respect to global macroeconomic conditions"), potentially reducing the magnitude and impact of the 2007-2008 oil shock.

A key feature of a speculative bubble is the attendant anomalous convergence of expectations that occurs when a growing share of investors believes that prices can only go up and that the risk of reversal somehow disappears... Shiller believes that convergence of expectations is a natural, endogenous phenomenon engendered by such things as a long-established benevolent economic environment and economic innovations announcing a new era of prosperity...They conclude,

However, a straightforward alternative is that monetary policy itself provided the anchor for the convergence of expectations, based on the consistent record that any decline in asset prices would be countered by the Federal Reserve with vigorous monetary expansion. Indeed, Alan Greenspan had just arrived at the Federal Reserve at the time of the 1987 stock market crash; he promptly reacted by aggressively lowering policy interest rates. He did it again in 1998 at the time of the LTCM crisis that followed the East Asian and Russian crisis, and even more aggressively after the end of the dot.com bubble in 2000. In all these episodes, there were no adverse effects of falling asset prices on economic activity and subsequently stock prices recovered.

The pattern is clear – the Fed repeatedly and systematically intervened to counter “negative bubbles”, while it remained passive when confronted with accelerating credit and asset prices. This policy approach, long established and clearly announced for over a decade, must have played an important role in bringing about convergent expectations of ever-rising asset prices, which eventually destabilised financial markets and the economy. Such an asymmetric monetary policy creates a gigantic moral hazard problem, whereby all agents expect to be rescued from their mistakes.

... the massive financial instability of 2007-8 was primarily the result of lax monetary policy, mainly in the US. The regulatory system compounded this error by tolerating excessive leverage and maturity transformation by banks in the US and Europe. Innovation did contribute to credit expansion and instability, but in all likelihood, without lax money and excessive leverage, reckless bets on asset price increases would have been much reduced.Finally, Simon Johnson calls on the Fed for an apology for its failure to even consider financial sector issues in its 2003 FOMC meetings:

[T]his and other FOMC transcripts make it clear that the senior Fed decision makers [in 2003] were not even thinking about the first order financial sector issues. They weren’t aware of what the big investment banks were really doing – show me the intelligence reports before the FOMC or the analytical discussion that indicated any degree of worry. No doubt someone somewhere in the Federal Reserve system was thinking critically about finance – feel free to send me any relevant details - but from the point of view of evaluating the institution, it only counts if the top decision-making body at least has the issues on the table.That is enough Fed smakckdown for one day.

[...]

I fully understand that financial market considerations are not the established focus of central bank interest rate deliberations. But the scope and nature of such deliberations has changed a great deal since the founding of the Fed almost 100 years ago. As the economy changes, central banks have to adapt their conceptual frameworks and our broader regulatory frameworks need to change also.

Huge problems were missed by people using anachronistic conceptual frameworks. Those frameworks should change... Our top monetary policy makers completely missed the true nature of the Great Bubble and its consequences, until it was far too late. They should apologize for that and we can start work on redesigning the institution, its decision-making, and how financial markets operate, to make sure it won’t happen again.

Martin Wolf's Counterfactual Question

Recently I had an interesting conversation with Martin Wolf of the Financial Times. We were discussing whether it was the Federal Reserve (Fed) or the saving glut from emerging markets that fueled the global liquidity glut in the early-to-mid 2000s. Martin Wolf argued it was the saving glut that was the important enabler and that the Fed's response was more or less an endogenous one. I, however, made the case that the Fed played an important role in creating the global liquidity glut given its monetary superpower status. By the end of the conversation our disagreements had narrowed, but one of the unresolved questions we ended on was whether the Fed could have acted differently given the political economy of the time. Here is Martin Wolf replying to me:

Yes, the Fed could have chosen otherwise, by a mixture of monetary and regulatory policies. I do not disagree. But to have done so would have meant a weaker recovery in domestic output. That might have been the right policy. But could it have got away with it? Who knows?So what do you think? Could this counterfactual have happened in the 2003-2005 period? As I have noted before, productivity and aggregate demand growth were robust during this time, suggesting tightening could have occurred without harming the recovery. On the other hand, employment growth was sluggish and the political push for increased home ownership would have made tightening politically challenging. Of course, the whole point of having an independent central bank is for moments like these, when tough calls have to be made.

Friday, August 7, 2009

Unconventional Monetary Policy Works After All

Scott Sumner alerts us to the fact that unconventional monetary policy is working in Great Britain and notes that had the United States followed suit there would have been far less need for a major fiscal stimulus package here. He points out that even Paul Krugman, who argued for a large fiscal policy because monetary policy was allegedly tapped out, is admitting as much. Here is Sumner:

A few months ago I got into a series of arguments with some old-styleKeynesians who kept insisting that monetary policy is ineffective once nominal rates hit zero. “Period. End of story.” I kept trying to explain that unconventional monetary policy could still be highly effective; the problem was that we needed to be much more aggressive. I pointed to FDR’s currency devaluation in1933 as an example of how an aggressive monetary policy could boost NGDP rapidly, even with interest rates near zero and much of the banking system shut down for months.Yes, we should have been more aggressive with monetary policy last year and less reliant on fiscal policy. For a primer on how unconventional monetary policy can be effective even when there is a liquidity trap see this piece from the BIS or this article from the NY Times. For empirical evidence that the Fed could have done more last year rather than sitting by and letting monetary policy effectively tighten see here.

Finally my views are getting some respect.... and now there is this post from the Time’s Nobel Prize winning columnist:Two months ago I wrote that there were hints of a relatively quick economic turnaround in Britain. Now those hints have gotten much stronger. Basically, aggressive monetary policy and the depreciation of the pound are giving Britain a boost relative to other advanced countries.If only the US had followed a similar course, instead of relying almost completely on costly fiscal expansion, which has only a modest impact on the path of NGDP over time. Still, it’s not too late for US to learn some lessons from the Brits.

Thursday, August 6, 2009

Assorted Musings

Here are some more assorted musings

- Since there are plenty of critical pieces on the economic policies of President Barrack Obama and Fed chairman Ben Bernanke, I think it is only fair to take a look at a few articles that discuss their performances in a balanced manner. To that end here is Jeff Frankel evaluating the Obama administration and here is Thomas Cooley apprasing the Bernanke Fed. Important points that come out from these pieces is that (1) one must consider worse alternative outcomes that could have emerged had certain policies not been adopted and (2) it is only reasonable to expect some policy mistakes be made in policy making when one is the heat of battle with little time to deliberate.

- As I have noted before, the Fed has some real challenges ahead of it once the recovery starts. Two recent Financial Times (FT) articles highlight some of these looming challenges. First, the FT reported that a large part of Wall Street's recent success is due to its trading with the Fed. These big banks apparently are selling overpriced securities to the Fed. The Fed is allowing this to happen to keep credit markets from freezing up. My question is how will these credit markets ever get weaned from the Fed? Second, the FT in another piece noted that in order for Bernanke to flawlessly execute his exit strategy he will need to have a good measure of the output gap. This metric, however, is not easy to measure, especially so during times of structural change such as the present. Some have argued this was one reason the Fed messed up on the 1970s--it misread the output gap and as a result was too expansionary. Will the Fed get it right this time?

- Dr. Doom (i.e. Nouriel Roubini) becomes Dr. Optimistic in this article where he looks at countries that are doing relatively well given the global recession. A key characteristic he finds among these countries is that they strove to balance their budgets over the business cycle. That is they ran policy such that they saved during the boom years so that they could more easily run accommodative policies during the bust years.

- Richard Thaler has an interesting Op-Ed in the Financial Times discussing how this crisis should be one of the final nails in the coffin of the efficient market hypothesis (EMH). He makes this point specifically with regards to the EMH implication that asset prices fully reflect all information and provide accurate signals about the fundamentals behind the assets. He noted that now that we have had the Japanese asset bubble in the late 1980s and the U.S. asset bubbles in the late 1990s and mid 2000s, the hard-core advocates of EMH have a lot of explaining to do:

So where does this leave us? Counting the earlier bubble in Japanese real estate, we have now had three enormous price distortions in recent memory. They led to misallocations of resources measured in the trillions and in the latest bubble, a global credit meltdown. If asset prices could be relied upon to always be "right", then these bubbles would not occur.

Monday, August 3, 2009

Sunday, August 2, 2009

More On the Importance of Nominal Spending Shocks

Scott Sumner has a new article that provides a nice follow up to my previous post where I argued that stabilizing nominal spending rather than inflation is the key to macroeconomic stability. Scott similarly argues that inflation targeting is a poor option for monetary policy compared to nominal income targeting. After reading his post, I was reminded of some quick and dirty empirical analysis I did on this blog that lends support to this view. Here is an excerpt:

The importance of stabilizing nominal spending can be seen in the graph below that plots the relationship between the output gap and nominal spending shocks. The output gap is calculated as the percent difference between actual real GDP and the U.S. Congressional Budget Office’s potential real GDP. The nominal spending shocks series is calculated as the deviation of the year-on-year growth rate of quarterly final sales to domestic purchasers from its preceding 10-year moving average. The data cover the period 1953:Q1 - 2008:Q1.The scatterplot makes it clear there is a strong, positive relationship between nominal spending shocks and the output gap. As a comparison, I have constructed in the same way an inflation shock series from the PCE price index and plotted it below against the output gap.These figures indicate nominal spending shocks are more closely related to the output gap than inflation shocks. Given these results, I went ahead and plugged the nominal spending shock and output gap series into a vector autoregression (VAR) to get a sense of their dynamic relationship. Five lags were used in the VAR, which is enough to remove serial correlation from the quarterly data (data already in growth rates so no unit roots). After estimating the model and imposing recursive ordering to identify the structural shocks, I got the following impulse response function (IRF) for the output gap given a 1 standard deviation shock to nominal spending:In plain English, the above figure shows that the typical shock to nominal spending leads to about a 0.5 percentage point increase in the output gap--a positive output gap--that persist for about a year and then begins unwinding. Another interesting exercise is to look at the decomposition of the forecast error from the VAR. This exercise explains how much of the forecast error can be attributed to a certain shock. (It tells us whether the interesting results from the IRF really matter)

Here we see that nominal spending shocks account for about 50% of output gap forecast error, a significant amount. By comparison, if the VAR is reestimated with the above inflation shock series instead of the nominal spending shock series, only about 8% of the forecast error can be explained by the inflation shock. Nominal spending shocks matter greatly!

Now I do want to oversell the findings presented here since they are based on a two variable VAR, but they are highly suggestive that nominal spending shocks are more important to macroeconomic stability than inflation shocks. Hence, monetary authorities should pay more attention to nominal spending. Moreover, stabilizing nominal spending should do better than inflation targeting at preventing the buildup of financial imbalances and asset bubbles for reasons explained here. In short, I am big believer that there would be meaningful gains in macroeconomic stability should the Fed should adopt a nominal income targeting rule.

{kind=link}

{kind=link}

Subscribe to:

Posts (Atom)