Bruce Bartlett has a new piece summarizing his views on what monetary policy can and can't do for the U.S. economy. Although no names are listed I suspect the excerpt below from his piece is directed to folks like Scott Sumner and me:

From the beginning of the crisis there have been economists who said that monetary policy was sufficient to stem the deflation and turn the economy around without fiscal stimulus. Just pump up the money supply, they said; that will stem the deflation all by itself and save the country from a destabilizing increase in debt, a lot of wasteful pork barrel spending, and avoid an implicit tax increase via Ricardian equivalence... The problem is that the Fed did increase the money supply a lot... Of course, there has been no inflation because deflation remains the economy’s central problem.That is because all the money created by the Fed never got spent; it just piled up in bank reserves. I explained this problem in my July 16 column. This was the fallacy of the monetarist view. Monetarists just assumed that increases in the money supply would be spent.While it is true that Scott Sumner and me have argued that there would be little need for fiscal policy had monetary policy been doing its job all along, no where have we said it was simply a case of further increases to the money supply. Rather we have been making a more nuanced case for further Fed action. Below is my reply to him.

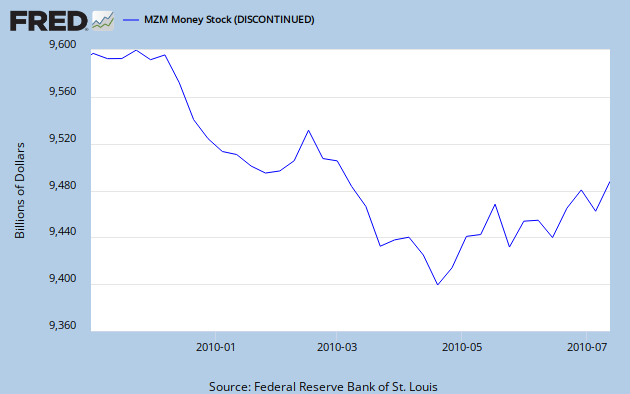

By the way, given the identity M=Bm we can see that technically the Fed has not increased the money supply a lot, it has only increased the monetary base a lot. In fact, if one looks at MZM or M3 they are actually down for the year.Bruce,

You underestimate the ability of the Fed to stabilize spending. Yes, the Fed has increased the monetary base with little to show but this is very different from what folks like Scott Sumner and me have been arguing. Nowhere have we said that further increases to the monetary base alone will cause everything to fall into place in the economy. Our message has been more nuanced than that. We have argued primarily for the Fed to adopt an explicit nominal target that would help shape expectations and thus stabilize velocity. We have also argued the Fed should abolish the interest paid on excess reserves and engage in further quantitative easing (i.e. expansion and alteration of the its balance sheet) as needed to hit its nominal target. Then, and only then, you would see some real traction.

Let me present our case--the way I see it anyhow--using the expanded equation of exchange. First take the regular equation of exchange, MV=PY (where M = money supply, V=velocity, and PY = nominal GDP or aggregate demand) and expand the money supply term, M, such that M=Bm where B = monetary base and m = money multiplier. This expanded version of the equation of exchange can be stated as follows:

BmV = PY

In this form, the equation says (1) the monetary base times (2) the money multiplier times (3) velocity equals (4) nominal GDP or total spending (i.e. aggregate demand). The Fed has complete control over the monetary base, B. It has less control over the money multiplier,m, but still can shape it to some degree as it is currently doing by paying banks interest payments to sit on excess reserves. (Imagine what might happen to m if the Fed started charging a penalty for holding excess reserves? We saw how excited the stock market got just at the idea of dropping interest paid on excess reserves.) The Fed can also influence V by setting an explicit nominal target (e.g. inflation, price level or nominal GDP target--the latter being my first choice). In short, the Fed has enough influence that if it really wanted to it could do much to stabilize BmV (or MV). And all of this could happen without resorting to more fiscal policy.

This is not just a theory. Christina Romer and others have shown it was the reason for the rapid recovery of 1933-1936. Have some faith Bruce. There is much moneary policy can still do.

{kind=link}

Update: Matthew Yglesias also responds to Bartlett.

Exactly! Why don't people understand that increasing the base money supply is not the same thing as increasing the money supply? This is especially true when you are suppressing the multiplier by paying banks to hold base money!

ReplyDeleteIt seems that a great many commentators assume that the quantity of base money that banks wish to hold is always less than the reserve ratio mandated by the Fed.