Everyone knows that deflation is a horrible thing: the price level declines, profits fall, employment drops, real debt burdens increase, households in turn spend less, prices fall again, and the cycle repeats. Folks like Paul Krugman, Greg Ip, and Barry Ritholtz have been reminding us of these dangers as there seems to be a greater chance that deflation could reemerge soon. David Leonhardt weighs in on this issue and notes that the sustained lack of inflation in the last two years is unprecedented in the postwar period, except for that "unusual" 1950s period:

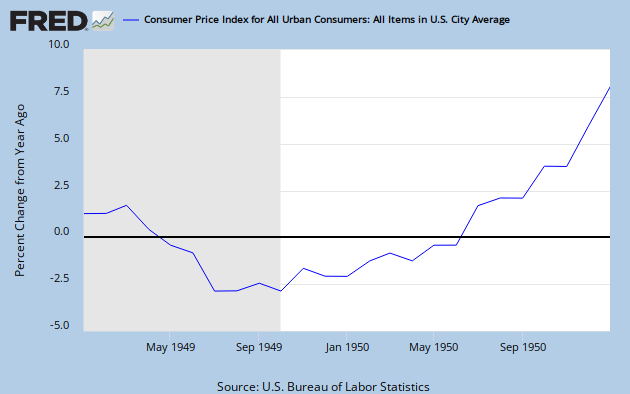

Since the Labor Department started keeping records in 1947, there have been only six six-month periods when prices have fallen more than [the past six months]. All of them were in 1950, an unusual time when prices were falling even though the economy was growing.

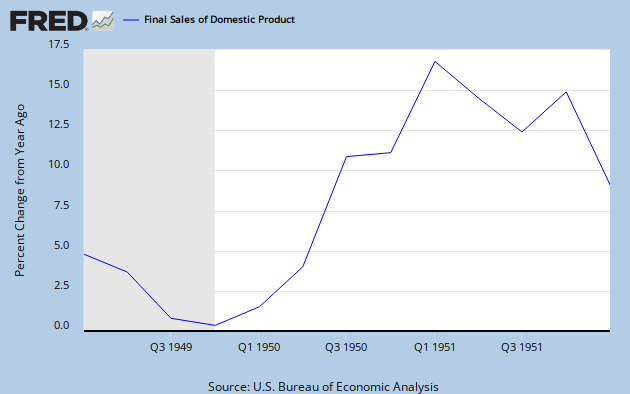

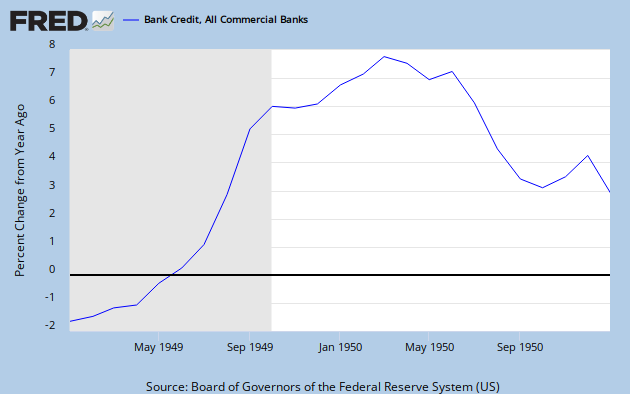

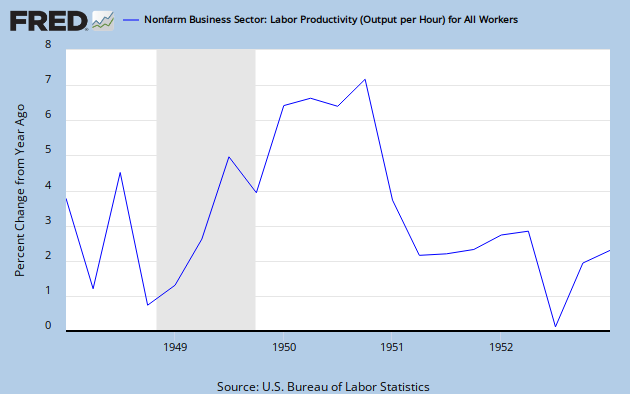

Gasp. How can it be? Deflation and a growing economy? There must be some mistake because observers like Paul, Greg, and Barry have told us this is impossible. Surely, Leonhardt misread the data. So what the does the data actually show? Let's see, the Fred database shows....gasp. It worse than Leonhardt reports. Looking at the year 1950--the first of these unusual six periods--one finds not only deflation but also solid growth in aggregate demand, corporate profits, employment, and financial intermediation. These developments are not suppose to happen with deflation! Oh my, how can this be? Maybe our high priest of central banking, Ben Bernanke, can shed some light on this mystery. He did, after all, make a famous speech in 2002 that touched on deflation. Now let's see, what did he said in that speech:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The sources of deflation are not a mystery. Deflation is in almost all cases a side effect of a collapse of aggregate demand--a drop in spending so severe that producers must cut prices on an ongoing basis in order to find buyers.(1) Likewise, the economic effects of a deflationary episode, for the most part, are similar to those of any other sharp decline in aggregate spending--namely, recession, rising unemployment, and financial stress.

Thanks Bernanke, but this analysis is not helpful. It is essentially the same thing said by Paul, Greg, and Barry and therefore does not shed any light on the 1950 deflation episode. But wait, Bernanke does have that footnote (1) above. Let's see what it says:

Conceivably, deflation could also be caused by a sudden, large expansion in aggregate supply arising, for example, from rapid gains in productivity and broadly declining costs. I don't know of any unambiguous example of a supply-side deflation, although China in recent years is a possible case. Note that a supply-side deflation would be associated with an economic boom rather than a recession.

Wow, now that is different. And wait, it is consistent with the 1950 deflation experience because there was a productivity boom then. Ok, now that the high priest has said it is possible to have deflation and robust economic growth let's think through the implications of such a productivity-driven deflation. First, laborers should not get shafted even if there are sticky wages. Their real wage should increase through the drop in the price level–workers’ purchasing power will rise. Second, firms' profits should not be harmed either since the productivity gains are lowering their per unit costs of production which offsets the fall in the output price. Third, any unexpected increases in real debt burdens should be matched by unexpected increases in real incomes–no debt deflation problems. Fourth, financial intermediation should not suffer since the productivity boom increases expected future earnings and thus assets prices (i.e. collateral values) go up–no balance sheet problems. Finally, the productivity surge should push up the real interest rate and provide an offset to the deflation drag on the nominal interest rates. Thus, the zero bound is unlikely to be a problem. Aggregate supply (AS)-induced deflation, then, is a lot different than aggregate demand (AD)-induced deflation.

{kind=link}

Clearly, the deflationary threat now facing the U.S. economy is of the AD-induced kind. I am concerned about it and have called on the Fed to be more responsive to this potential threat. With that said, this deflation distinction is more than some trivial academic argument. It helps shed light on why the Fed's decision to keep interest rates so low for so long were disastrous in the early-to-mid 2000s. The Fed saw sustained disinflation and and assumed it was the result of faltering AD. The data is now very clear that the deflationary pressures were more the result of the 2002-2004 productivity boom. The productivity boom implied inflation should have been lower, the neutral interest rate higher, and the economic recovery was not in jeopardy. The Fed thought otherwise and, as a result, helped fuel one of the largest credit and housing booms in history. The irony in all of this is that the Fed's fear of deflation in 2002-2004 caused it to act in a manner that help put in a motion a cumulative process that is likely to create the very thing it was trying to avoid in the first place: deflation. Know your deflations!

Update: Some folks have noted that there were several recessions in the 1950s associated with deflation. Great, but that is not what I am getting at here. Most everyone can tell a story about how recessions can create deflationary pressures. Few, however, have an easy time accepting that an economic expansion can also occur with deflation. My focus here was on just the 1950-1951 episode--a clear cut case of the latter. Pointing to the other 1950 episodes is besides the point because they are of the former kind and easy to explain.

{kind=link}

Update: Some folks have noted that there were several recessions in the 1950s associated with deflation. Great, but that is not what I am getting at here. Most everyone can tell a story about how recessions can create deflationary pressures. Few, however, have an easy time accepting that an economic expansion can also occur with deflation. My focus here was on just the 1950-1951 episode--a clear cut case of the latter. Pointing to the other 1950 episodes is besides the point because they are of the former kind and easy to explain.

It seems that by the way money enters the economy, i.e. through loans, too much gets funneled into housing right off the top, which also increases the value of housing in relation to other portions of the economy. Now, with the price of housing coming down, other assets appear to be declining in value but that kind of deflation seems to be primarily in secondary markets where production capital is currently underutilized.

ReplyDeleteThe 1950 episode may be of academic interest, but it was brief, and who knows if measuring inflation is even accurate when gets down to the low zero-onesy-twosy range.

ReplyDeleteI presume there was strong AD in 1950. You also get declining overhead per unit costs when AD is strong and growing. (That's one reason why stimulus is not as inflationary as imagined by the current timid Japan Wing of the Fed).

The 1950 episode is trivial in light of today's situation in the USA, or the 20-year-long track record in Japan.

Now we need agressive QE and other Fed actions. We need to reflate property values, and deleverage.

The dithering Japan Wing of the Fed needs to be slapped down, or given a shot of whiskey and a shot of testosterone.

Benjamin,

ReplyDeleteI agree it is has no bearing on today's problems, but couldn't resist responding to Leonhardt's apparent puzzlement over this period. Don't worry I am still concerned about the real deflation problem now.

Benjamin says: "We need to reflate property values". Own a home that's $200K underwater do we ?

ReplyDeleteI think DB had a much better idea when he suggested a debt to equity swap for home mortgages.

Your point about deflation and growth is well made. It reminds me of Adam Posen's recent paper on Japan ("Neither Ran nor Rashomon"). Basically he points out that Japan's productivity and GDP growth were pretty good, despite having persistent mild deflation.

ReplyDeleteThe dilemma he poses is if the output gap was shallow, then deflation should have not been so persistent. But if it was high, deflation should have accelerated over time.

Some people (such as Scott Grannis) are now saying that because Japan's deflation was not tragic, that it is OK for the US. American households are far too leveraged to endure deflation I would guess.

But back to Posner... he attributes the Japanese experience in part to the central bank lacking resolve and not having much credibility amongst market participants. Given the hesitating and disunited Fed, it seems like we are reaching that point.

Think they were more concerned about the unemployment than the disinflation?

ReplyDeleteECB-Please argue issues on the merits.

ReplyDeleteActually, I own industrial that is still well abovewater.

That said, any investor of any stripe in this economy needs reflation. There is no sin in property investors smelling profits and getting back to investing.

And, it is a reality that banks have lent on property based on nominal dollars. If we can reflate, and inflate generally, those loans, at least more of them, can be made good. Japan never got over this hump. Their property and equity values are dwon 75 percent in the last 20 years.

Yet Japan central bankers still pettifog about inflation.

Chris-Japan's GDP growth has been awful over the last 20 years. Below that of statist France, on a per capita-GDP basis. Rotten record.

As for an aging workforce--some say Japan's dearth of young is being caused by a bad economy. No one can afford kids. It is sad.

If you herry-pick certrain start dates, and strtech certain numbers on a per workjer basis, you can show Japan bumbled through at best.

But the real record of Japan is that tight money, a strong currency and zero inflation-deflation has produced misery, misery, misery.

Only a very strong culture, low crime rates, and a generaly pro-business culture has allowed Japan to not prosper, but bumble through.

The point is not comparing GDP in Japan to other countries, actually. The point is that it is an open question, why deflation occured during periods of growth in Japan. That's the issue.

ReplyDeleteWhat Posen says, is that in the cyclical expansion from 2002-2008, Japan had the high GDP growth and very high productivity growth during the period. Higher by either measure than the US, UK, Germany, or France. Yet during this period, Japan went through deflation.

So, the real question for the USA is whether a cyclical recovery will banish deflation here. That's the question both Posen and David Beckworth are getting at. Since I had just finished with Posen's paper, I though it might be of interest to either David or his readers.

You might find it interesting -- I certainly learned a few things.

If there is an AS shock, should there be price inflating with currency instead of debt?

ReplyDelete