1. Like the monetarists, we tend to analyze AD shocks through the perspective of shifts in the supply and demand for money, rather than the components of expenditure (C+I+G+NX). And we view nominal rates as an unreliable indicator of the stance of monetary policy. We are also skeptical of the view that monetary policy becomes ineffective at near-zero rates.

2. Unlike monetarists, we don’t tend to assume the demand for money is stable, and are skeptical of money supply targeting rules.

As I noted before, quasi-monetarists are not that different from other folks who see an AD problem in the economy. One defining difference, though, is that quasi-monetarists see the insufficient AD issue ultimately as an excess-money demand problem and believe the Fed could meaningfully address it. Another defining difference is that quasi-monetarists were calling for more Fed action long before it was vogue. Thus, early on in the recession when other folks were calling for fiscal policy to address the AD problem, quasi-monetarists were instead calling for the Fed to step up and address the fall in nominal spending.

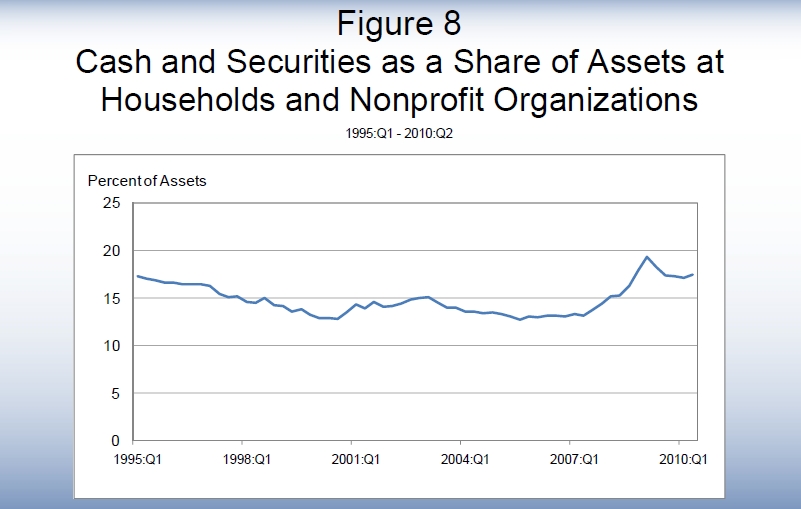

Does the quasi-monetarist's emphasis on excess money demand have any merit? Is there any evidence that the AD problem is ultimately an excess money demand problem? Drawing on Gary Gorton's work that shows repos are a form of money--an understanding supported by the fact the now discontinued M3 money supply included repos--for the shadow banking system, the blogger 123 presents evidence from a natural experiment around the time of the Lehman collapse that shows there was a sudden spike in the demand for money. Below are charts that present further evidence that there has been an elevated increase in the holdings of cash and other highly liquid (i.e. cash equivalent) securities by households, businesses, and banks. These charts come from Eric Rosengren's recent speech: (Click on figures to enlarge.)

{kind=link}

Though Eric Rosengren does not call himself a quasi-monetarist, his speech is consistent with this view: it argues there is a AD problem, it shows the above graphs that indicate an elevated increase in money demand, and it calls for more aggressive Fed action to address these problems. Rosengren's implicit endorsement of the quasi-monetarist's view is probably not unique. I suspect most folks who see the need for more Fed action would, after some reflection on the excess money demand take on the AD problem, consider themselves a quasi-monetarist. Are you?

MV=PQ or Y=C+I+G. I'll take neither. We can always portray our current downturn in terms of these aggregates since they are tautologies. But neither has any utility in actually understanding what is happening. They are both demand stories, and America's problems are supply-side. And they did not start with Lehman or "tight money". America's potential GDP growth rate has been falling some time now, partly due to a failed education system, inappropriate govt intervention in housing, excessive military spending and a regulatory failure in the financial system brought about by a corrupted political system.

ReplyDeleteMonetary policy's role was to paper over the cracks post-2000 tech crash, but it is not a causal factor in America's deep-seated and long-running structural problems. Over the long span of history, bad monetary policy has almost always occurred as the product of underlying political problems. It is a symptom of deeper political tensions, interest group fights over distribution of a shrinking pie, a means of creating an illusion of wealth for a once great nation that is steadily seeing its production possibilities curve moving inward.

How should we conduct monetary policy to minimize disruption to the economy? Targeting NGDP sounds like a good idea. But it seems that quasi-monetarists have a strong view of the relevance of macroeconomic policy to our economic troubles. This is my issue. I see little evidence that tight money caused the recession and see little reason to expect that QE2 will speed recovery in a significant way. The benefits are mostly psychological.

ReplyDeleteWe are experiencing an Austrian recession. This does not mean the Austrians have a valid general model of the business cycle. But in this case we have a recession caused by government stimulated mal-investment on an epic scale. Tight money didn't cause this recession and easy money won't fix it.

Arguments that unemployment is cyclical and not structural are not persuasive either. We have a structural shift from consumption of all kinds to investment. Consumption is down. Savings is up but there are few investment opportunities, in part because consumption is down and in part because we have the most hostile political environment for investment since the 30s. People are holding on to cash, not because they are spooked, but because there is no place to invest.

Saving is up and consumption is down requires a lower real interest rate to keep the amount saved and amount invested balanced. Oddly enough, in this situation, these changes are offsetting in terms of the composition of demand and allocation of resources. There is less need for structural unemployment than otherwise. (My view is that there needs to be a shift from residential housing to other sorts of investment so I do see a large structural element.)

ReplyDeleteTo the degree that needed decrease in the real interest rate is inconsistent with basing the financial system on zero-interest bearing non (or low) inflationary fiat currency, then these changes in saving or investment have monetary effects--reduced money expenditures. If money prices for goods or resources (like labor) are sticky, then real expenditures will be impacted.

The notion that added saving and reduced investment necessarily reduces real expenditures is in error.