I have a new article up at National Review Online where I argue that the best way for Congress to narrow the Fed's mandate is through nominal GDP level targeting. One point mentioned in the piece is that because a nominal GDP target ignores aggregate supply shocks it dominates an inflation target. This applies equally well to a price level target. Another way of thinking about this is that movement in the price level is a symptom of all underlying shocks, whereas movement in nominal spending is an underlying shock itself (i.e. an aggregate demand shock). The Fed will be far more effective if responds directly to the underlying shock over which it has influence--the aggregate demand shock--than responding indirectly to an imprecise symptom of that shock.

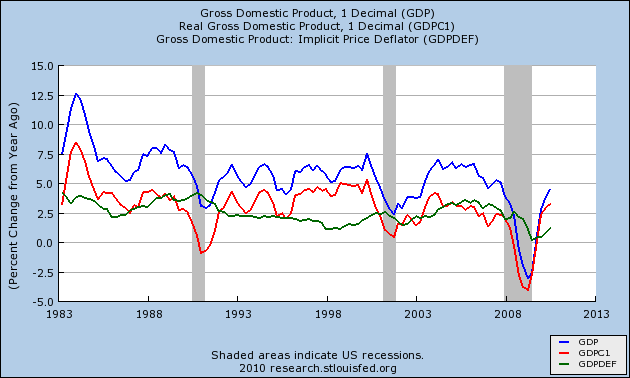

The importance of nominal spending shocks can be seen in the three figures below. The first figure shows the growth rates of nominal GDP with the blue line, real GDP with the red line, and the GDP deflator (i.e. inflation) with the green line. The figure reveals that changes in nominal spending get translated largely into changes in real economic activity. (See Marcus Nunes for more analysis on this figure.)

The next figure shows the relationship between a crude measure of nominal GDP shocks and the output gap for the period 1957:Q1-2010:Q4. The shock is calculated as the difference between the year-on-year growth rate of nominal GDP and a rolling 10-year average of the year-on-year nominal GDP growth rate. The idea here is that the 10-year rolling average provides a forecast for the current nominal GDP growth rate. Any deviation from that forecast is a shock. Here is the figure:

The figure shows a remarkably close relationship between nominal spending shocks and the 1-quarter lag output gap. The same shock series is then constructed for the GDP deflator and plotted against the lagged output gap. Here is the result:

Price level shocks are barely related over this long sample. If anything the nominal GDP shock series probably understates the importance the shocks given how crudely they are constructed But the point is made: it makes more sense for the Fed to target the nominal GDP level than inflation or the price level.

For more on nominal GDP targeting see these previous posts:

This is really interesting.

ReplyDeleteHowever, asking Congress to refine the Fed's mandate, while Ron Paul is in charge of the relevant House committee...does the Gong Show come to mind?

The Wizards of the Fed could never admit that their job is so staggeringly simple.

ReplyDeleteGreat article.

ReplyDeleteAs usual, though, you get the brain dead people posting comments. People who would fail any monetary economics course.

To people who criticize the NGDP targeting idea, I always like to say: what is your idea? Monetary policy isn't something you can just walk away from. It's not like fiscal policy where you say, 'okay, I want the government to do this and this and this, and balance the budget'.

What are the alternatives to NGDP targeting? Inflation targeting? Some sort of gold standard? What gold standard? Details?

I want a monetary policy that targets nominal GDP. What exactly do you want?