David assumes that the the signaling effect would be enough to raise companies’ demand for loans, and that this would raise banks’ net interest margins (meaning that banks wouldn’t have to play the MMF funding/excess reserves arbitrage). Even if he is right, this would surely take time, whereas an MMF breaking the buck or a run on MMFs by nervous investors can happen extremely quickly. See: 2008, September.

As RBC analysts write, because short-term effective rates would unlink from policy target rates — ie all short-term rates would fast plunge to zero, and yes this kind of unmooring has happened before — such a move could “completely stop the volume of transactions in the Fed funds market, creating chaos in the derivatives and the floating rate note markets.”

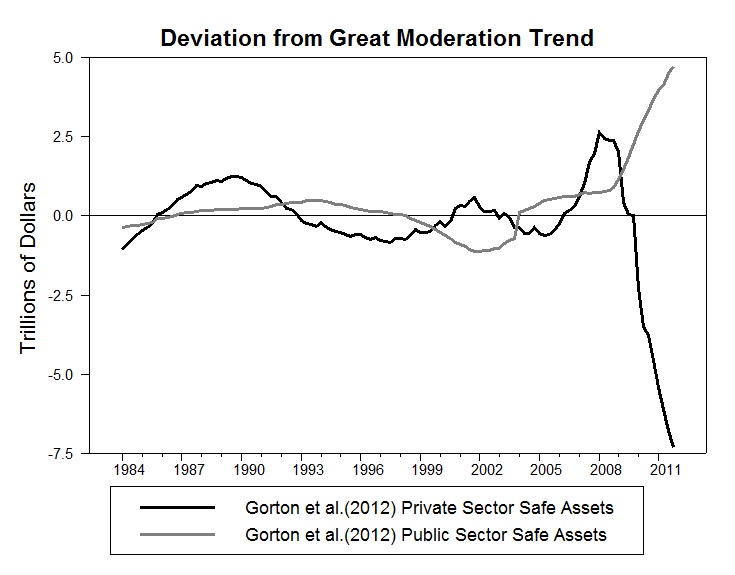

[...]

Again these scenarios could play out very quickly, and we think it’s reasonable to assume that disfunction in these markets is unlikely to be either mild or contained. How certain can we be that the signaling effect posited by David would be so instantly accepted by markets that it would either preclude the above scenarios or otherwise mitigate the risks they present?

Note that the premise for these dire scenarios is an ongoing weak economy with few safe asset alternatives for overnight funding markets. Lowering the IOER is not assumed to meaningfully change any of that in the near term. The key issue, then, is whether the Fed can generate a shock big enough such that it causes firms, households, and governments to immediately start wanting more financial intermediation services.

FDR showed that is possible in 1933 by abandoning gold. It required, though, a radical departure from the status quo, a sharp slap to the maket's face, a regime change. When FDR did it, it was a huge shock to market psychology as noted by Gautti Eggertson:

It is hard to overstate how radical the regime change was. “This is the end of Western civilization,” declared Director of the Budget Lewis Douglas. During Roosevelt’s first year in office, several senior government officials resigned in protest. These policies violated three almost universally accepted policy dogmas of the time: (a) the gold standard, (b) the principle of balanced budget, and (c) the commitment to small government. Interestingly, the end of the gold standard and the monetary and fiscal expansion were largely unexpected, since all these policies violated the Democratic presidential platform.

The equivalent today would something radical enough to throw the Ron Pauls of the world into a conniption fit. I think the abandonment of inflation targeting for something like NGDP level targeting via open-ended QE would do it. The problem with this is that such a regime change seems politically unlikely. And it that case, Cardiff Garcia's premise may be reasonable. Incremental policy changes may do more damage than good.

Update: Peter Ireland has the best formal treatment of IOER.

Update: Peter Ireland has the best formal treatment of IOER.