Scott Sumner is right. Brexit is the biggest global monetary shock since 2008. This could be the tipping point that turns the existing global slowdown of 2016 into a global recession. Here is why.

First, Brexit is adding further strength to an already overvalued dollar. The trade weighted dollar had appreciated roughly 25 percent between mid-2015 and early-2016. That is a very sharp increase in so short a time. It has come down some, but not much as seen in the figure below (red line):

The figure also shows that this sudden increase in the dollar is closely tied to the policy divergence between the Fed and the ECB (blue line). That is, as the Fed began talking up interest rate hikes in mid-2014 the ECB was talking up the easing of monetary policy. The rise in the blue line shows this policy divergence1

Brexit is now adding fuel to this dollar fire. The dollar has appreciated almost 4 percent since the Brexit fate became clear last evening, as seen in the figure below.

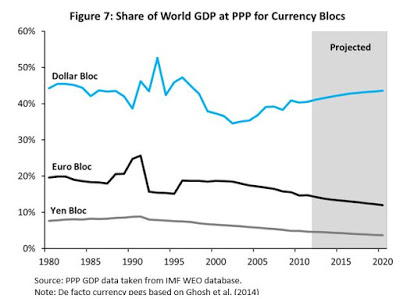

Why does a strengthening dollar matter? There are two reasons. First, over 40 percent of the world economy ties its currency to the dollar in some form. This can be seen in the figure below. That means when the dollar strengthens, these currencies strengthen too. This is the curse of the so called 'dollar block' countries--they import their monetary policy from abroad. Via this channel, Brexit has just further tightened monetary conditions in all these countries. This added pressure makes it likely China will be forced to devalue soon. And we saw how well that went last time it was tried.

The second reason the rising dollar matters is the rapid growth of what the BIS calls the 'parallel dollar system'. This is a system of dollar loans and dollar debt securities that has emerged outside the United States. This dollar credit to and from non-U.S. residents has tripled since 2000, while non-resident Euro and Yen financing has remained relatively stable. In fact, the dollar's share of this non-resident credit growth has increased from 62% to 75% according to BIS data. This means there is a lot of dollar-denominated debt outside the United States that is very vulnerable to dollar shocks. Brexit just increased the real debt burden of these borrowers.

So between tightening monetary conditions for the dollar bloc countries and increasing real debt burdens for all the non-resident issuers of dollar debt, the global economy has been hit with a large dollar shock. Put more crudely, the strong dollar noose that has been choking emerging economies since mid-2014 has now been complemented by the opening of trap door on the gallows via Brexit. This makes the strangulation of global economy complete.

A second reason Brexit might be pushing the global economy into a global recession is that it hastening the the frantic race to bottom on safe yields. As I noted in a recent post, yields on safe assets around the world have been going down since the demand for safe assets remain unmet. Given global capital markets this also means there is a race to the bottom on safe yields as noted by Caballero, Fahri, and Gourinchas (2016) :

In the open economy, the scarcity of safe assets spreads from one country to the other via the capital account. Net safe asset producers export these assets to net safe asset absorbers until interest rates are equalized across countries. As the global scarcity of safe assets intensifies, interest rates drop and capital flows increase to restore equilibrium in global and local safe asset markets. Once the ZLB is reached, output becomes the adjustment variable again.

Brexit massively intensified this race to the bottom as seen in the the 10-year yield below. Incredibly, the yield fell from 1.74 to 1.43 this evening! Brexit, in other words, just jolted the demand for safe, liquid assets in a major way.

This frantic race to the bottom of safe yields will eventually run up against the effective lower bound (ELB). When that happens something else will have to adjust. And that something is output, as noted by Caballero, Fahri, and Gourinchas (2016)

So there you have it. The world has been hit with a massive global monetary shock. And via dollar bloc countries, the parallel dollar system, and the shortage of safe asset problem this monetary shock may be what pushes an already slowing global economy into a global recession.

Will central bankers and finance ministries be ready for it? I hope so.

Update: For some soul searching on the why of Brexit, see my previous post.

1The blue line shows the spread between the 1-year US treasury rate and the 1-year Euro rate. Based on the expectation hypothesis, the 1-year interest rate approximately equals the expected average of short-term interest rates over the same horizon. Consequently, if 1-year rates are going up it implies short-term rates are expected to rise on average over the next year. The spread between the treasury and euro rates, then, reveals the expected divergence between the expected path of policy interest rates over the next year.

Professor Beckworth- Are exchange rates as important as you suggest? My initial reaction is that it only impacts the export-import variable in any given countries' NGDP. And any decline in exports - imports (through both increased imports and declining exports) could be offset to some degree by higher purchasing power-> cheaper goods-> movement along the demand curve within the country with the stronger 'dollar' = more consumption. That is to say, it is not a 1 to 1 fall in NGDP for the decrease in export-imports. Maybe the answer is it depends on the country and the ability to adjust in the real economy or perhaps I'm totally off base (usually the case).

ReplyDeleteProvocative and informative, as usual. Would it be right to characterize your view about the underlying causes of the safe asset shortage as follows?

ReplyDeleteTight monetary policies--on the part of various central banks with varying degrees of linkage to the Fed--effectively impose price controls on safe assets denominated in their respective currencies. These effective price controls operate directly on a certain class of public, short-maturity assets for the most part. But due to quasi-arbitrage with other safe asset classes--public and private, short and long maturity--the shortage leaks into other markets (I'm curious about the details of this mechanism).

And besides this leakage problem, the destabilization of long-term macro (NGDP) expectations due to bad monetary policy both makes it tougher to privately produce safe assets by increasing credit spreads and also increases the demand for safe assets.

Eric, the idea behind the race to bottom is that as yields on one safe asset get driven to the lower effective bound investors will look elsewhere until all safe asset yields hit their bottom. The price control is the institutional constraint of the effective lower bound where investors would rather hold cash. Here is a post from a few months ago where I dig a little deeper into this problem. You may find it useful.

DeleteThis comment has been removed by the author.

DeleteFrankly, I am not seeing it. I suspect this will be old news in a couple of weeks and everybody moved on. A bunch of weak moves won't matter. It will unwind and we will be back to where we where yesterday.

ReplyDeleteSure, England will become weaker and Scotland will flee back to the EU. The Tories who voted "Leave" will regret it and reverse positions while socialist use the chance to make a "self-sufficient" hive in England while practicing xenophobia.

But markets move on.

Uhm, yes, markets did move on today but in a rather violent way.

DeleteMeh, not impressed. Markets will move on. Brexit probably isn't going to happen anytime soon. Maybe in 5 years. Maybe in 10 years. The Tories have always been pro-EU. They just wanted a better deal. Might be time to understand how fake this is.

Delete"Will central bankers be ready for this recession from this monetary shock?"

ReplyDeleteYes, I'm absolutely sure they will be. Because, as we all know, the world is not allowed to have an actual recession anymore. Good freaking grief!

"This is the curse of the so called 'dollar block' countries--they import their monetary policy from abroad. Via this channel, Brexit has just further tightened monetary conditions in all these countries."

ReplyDeleteCould you explain why making the dollar stronger tightens monetary conditions in these countries?

I think this is because of the interest rate parity condition: r = r* + 'delta e', where 'delta e' is the change in the nominal exchange rate defined as local currency per USD, r* is the Fed funds rate, and r is the domestic policy rate. The way e is defined implies that e going up equals a depreciation of the local currency -say the currency of one of the 'dollar block' countries-. In this case, since the dollar has strengthened vis-a-vis the pound, the domestic currency of other countries have depreciated vis-a-vis the dollar. So 'delta e' is positive, and if r* is constant, that means r goes up. In other words, a stronger dollar tightens monetary policy conditions in countries tied to the dollar.

Delete"Will central bankers and finance ministries be ready for it? I hope so." But you don't expect so, and neither do the markets. Central bankers and finance ministries are being given another opportunity to display their incompetence.

ReplyDeleteYes, Liaquat Ahamed needs to write Lords of Finance II covering the last eight years.

DeleteIn an open economy with a current account deficit the market clearing or equilibrium interest rate is the rate that attracts sufficient foreign capital to finance the deficit with a stable currency. If the currency is rising it is a signal that domestic interest rates and/or international rate spreads are too high.

ReplyDeleteOne problem with economic stagnation is that it is harder to absorb negative shocks. If trend growth is 4% and you are hit with a negative 2% shock, growth is still 2% and the economy has the momentum to carry through the shock and keep growing. But if trend growth is 2% and you are hit with a 2% shock, growth falls to 0% and it is harder to sustain growth. A 2% real growth world is a lot more dangerous than a 4% growth world.

"The second reason the rising dollar matters is the rapid growth of what the BIS calls the 'parallel dollar system'. This is a system of dollar loans and dollar debt securities that has emerged outside the United States"

ReplyDeleteIt was called the Eurodollar system for decades - whether the dollar instruments are domiciled in Europe, the Far East, the Bahamas, or anywhere outside the US ...

Has that terminology been retired?

(I must admit I don't see it much anymore)

Thanks David. I guess what will jolt the global market next will be a big devaluation of Yuan maybe? Also, I don't understand the relationship between race to the bottom on safe yields or safe asset shortage problem and output adjustment. Why does output have to be an adjustment variable in this case? Thanks.

ReplyDeleteDavid--

ReplyDeleteI blog about you and Raghuram Rajan over at Historinhas.

Thanks!

DeleteThis comment has been removed by the author.

ReplyDelete