One of the remarkable features of the U.S. recession has been the dramatic collapse in demand. This collapse has yet to fully recover, but progress is being made as can be seen in the following figure. This figure shows the year-on-year growth rate of U.S. domestic demand (click on figure to enlarge):

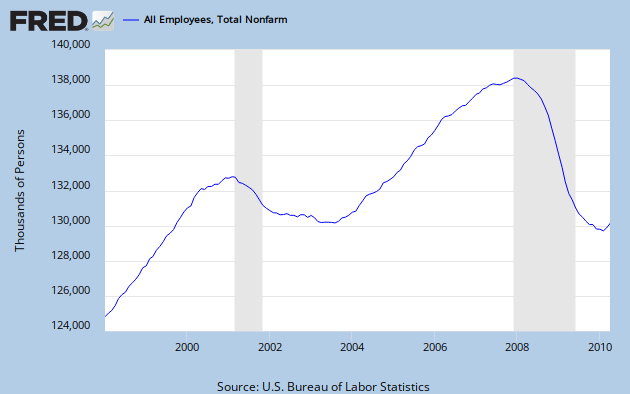

Given this modest recovery in demand one would think there would be a similar recovery in the labor market. But alas, unemployment remains stuck near 10% and the level of employment is where it was back in1999. Some observers are now wondering if more than demand is behind this lack of recovery in labor markets. Ryan Avent, for example, makes this point in a recent article in The Economist:

The acceleration of the labor productivity growth rate over the last few quarters is striking and consistent with Rampell's story. A more thorough measure, though, of productivity is total factor productivity (TFP) which the BLS only puts out on an annual basis. Fortunately, John Fernald of the San Francisco Fed has a paper where he constructs quarterly a TFP series as well as a utilization-adjusted (i.e. cyclically adjusted) quarterly TFP series. Unlike labor productivity which goes through 2010:Q1, the TFP data only goes through 2009:Q3. Still, an interesting picture emerges as seen in the figure below which graphs this data (click on figure to enlarge):

The acceleration of the labor productivity growth rate over the last few quarters is striking and consistent with Rampell's story. A more thorough measure, though, of productivity is total factor productivity (TFP) which the BLS only puts out on an annual basis. Fortunately, John Fernald of the San Francisco Fed has a paper where he constructs quarterly a TFP series as well as a utilization-adjusted (i.e. cyclically adjusted) quarterly TFP series. Unlike labor productivity which goes through 2010:Q1, the TFP data only goes through 2009:Q3. Still, an interesting picture emerges as seen in the figure below which graphs this data (click on figure to enlarge):

Overall TFP declined in the recession and has slightly recovered through 2009:Q3. It will be interesting to see if TFP recovers as rapidly as labor productivity in the subsequent quarters. My guess is that it will given the dramatic increase in utilization-adjusted TFP. Of course, this spike may be a one-time blip rather than a sustained increase. And unlike the productivity boom of 2001-2004, I don't know of any good stories for this spike in productivity. Still, it appears to be happening and this implies there may be more structural unemployment.

Overall TFP declined in the recession and has slightly recovered through 2009:Q3. It will be interesting to see if TFP recovers as rapidly as labor productivity in the subsequent quarters. My guess is that it will given the dramatic increase in utilization-adjusted TFP. Of course, this spike may be a one-time blip rather than a sustained increase. And unlike the productivity boom of 2001-2004, I don't know of any good stories for this spike in productivity. Still, it appears to be happening and this implies there may be more structural unemployment.

Given that there is structural unemployment, traditional unemployment benefits will not be a long-term solution. As Rampell notes,

Update: John Fernald along with Susanto Basu and Miles Kimball have a 2006 AER article titled "Are Technology Improvements Contractionary?" Here is the abstract:

Given this modest recovery in demand one would think there would be a similar recovery in the labor market. But alas, unemployment remains stuck near 10% and the level of employment is where it was back in1999. Some observers are now wondering if more than demand is behind this lack of recovery in labor markets. Ryan Avent, for example, makes this point in a recent article in The Economist:

{kind=link}

{kind=link}

Were demand all that mattered, employment would be stronger. But its weakness, taken with the divergence of hiring and vacancies, suggests that other explanations are needed. It looks increasingly likely that America’s labour market has developed structural problems that may explain why it is struggling to respond.Others making this argument include Tyler Cowen and Arnold Kling. Their bottom line is that in this current recession there is limit to what stabilizing demand--my preferred goal for monetary policy--can do for unemployment. In short, not all of the unemployment may be cyclical, some of it may also be structural. This point was further advanced a few days ago by Catherine Rampell in a New York Times piece. Among other things, Rampell brought up the fact that the rapid productivity gains occurring now imply more structural unemployment:

Pruning relatively less-efficient employees like clerks and travel agents, whose work can be done more cheaply by computers or workers abroad, makes American businesses more efficient. Year over year, productivity growth was at its highest level in over 50 years last quarter, pushing corporate profits to record highs and helping the economy grow...Now there are other developments besides productivity gains that may be increasing structural unemployment. For example, Ryan Avent points out that this recession has had an inordinate impact on employment in certain industries like construction and many households cannot move to find work because they are underwater with their mortgages. I want to focus, however, on Rampell's point that productivity gains may be creating more structural unemployment. If true it would require significant economy-wide productivity gains. So is there any evidence of this? Below is a figure of the year-on-year labor productivity growth rate (click on figure to enlarge):Millions of workers who have already been unemployed for months, if not years, will most likely remain that way even as the overall job market continues to improve, economists say. The occupations they worked in, and the skills they currently possess, are never coming back in style. And the demand for new types of skills moves a lot more quickly than workers — especially older and less mobile workers — are able to retrain and gain those skills.

The acceleration of the labor productivity growth rate over the last few quarters is striking and consistent with Rampell's story. A more thorough measure, though, of productivity is total factor productivity (TFP) which the BLS only puts out on an annual basis. Fortunately, John Fernald of the San Francisco Fed has a paper where he constructs quarterly a TFP series as well as a utilization-adjusted (i.e. cyclically adjusted) quarterly TFP series. Unlike labor productivity which goes through 2010:Q1, the TFP data only goes through 2009:Q3. Still, an interesting picture emerges as seen in the figure below which graphs this data (click on figure to enlarge):

The acceleration of the labor productivity growth rate over the last few quarters is striking and consistent with Rampell's story. A more thorough measure, though, of productivity is total factor productivity (TFP) which the BLS only puts out on an annual basis. Fortunately, John Fernald of the San Francisco Fed has a paper where he constructs quarterly a TFP series as well as a utilization-adjusted (i.e. cyclically adjusted) quarterly TFP series. Unlike labor productivity which goes through 2010:Q1, the TFP data only goes through 2009:Q3. Still, an interesting picture emerges as seen in the figure below which graphs this data (click on figure to enlarge): Overall TFP declined in the recession and has slightly recovered through 2009:Q3. It will be interesting to see if TFP recovers as rapidly as labor productivity in the subsequent quarters. My guess is that it will given the dramatic increase in utilization-adjusted TFP. Of course, this spike may be a one-time blip rather than a sustained increase. And unlike the productivity boom of 2001-2004, I don't know of any good stories for this spike in productivity. Still, it appears to be happening and this implies there may be more structural unemployment.

Overall TFP declined in the recession and has slightly recovered through 2009:Q3. It will be interesting to see if TFP recovers as rapidly as labor productivity in the subsequent quarters. My guess is that it will given the dramatic increase in utilization-adjusted TFP. Of course, this spike may be a one-time blip rather than a sustained increase. And unlike the productivity boom of 2001-2004, I don't know of any good stories for this spike in productivity. Still, it appears to be happening and this implies there may be more structural unemployment.Given that there is structural unemployment, traditional unemployment benefits will not be a long-term solution. As Rampell notes,

There is no easy policy solution for helping the people left behind. The usual unemployment measures — like jobless benefits and food stamps — can serve as temporary palliatives, but they cannot make workers’ skills relevant again.What can be done for these folks? Adam Ozimek proposes creating unemployment benefits that address structural unemployment:

So what policies could we pass to make the unemployed better off and incentive them in a way that speeds up the structural unemployment adjustment process? One idea is relocation vouchers. If you offer relocation vouchers to unemployed workers who move a minimum distance from their current residence, then you could incentivize labor to move where it is needed away from where it is no longer needed.This is an interesting idea and Ozimek provides further discussion on how to finance it. Since the evidence seems to point to increased structural unemployment it is worth rethinking how we do unemployment benefits.

Update: John Fernald along with Susanto Basu and Miles Kimball have a 2006 AER article titled "Are Technology Improvements Contractionary?" Here is the abstract:

Yes. We construct a measure of aggregate technology change, controlling for aggregation effects, varying utilization of capital and labor, nonconstant returns, and imperfect competition. On impact, when technology improves, input use and nonresidential investment fall sharply. Output changes little. With a lag of several years, inputs and investment return to normal and output rises strongly. The standard one-sector real-business-cycle model is not consistent with this evidence. The evidence is consistent, however, with simple sticky-price models, which predict the results we find: when technology improves, inputs and investment generally fall in the short run, and output itself may also fall.Technology here is analogous to TFP. This study, therefore, provides another reason to believe the rapid productivity gains of late may be creating structural unemployment.

Interesting posting. 250 years of history gives fair warning that, so great are the intertemporal coordination problems of a market system, the private sector is frequently unable to generate enough jobs. Maybe we will have to think about a job guarantee scheme as outlined by Minsky many years ago. I think they tried something like that in Argentina after the crash of 2001 and as far as I know it proved quite successful.

ReplyDeleteSo, we had 5 straight quarters of negative y-o-y growth of aggregate demand beginning with the 4th Q of 2008 through the 4th Q of 2009 and only in the 1st Q of 2010 has it been positive and already people are wondering why the labor market has not rebounded yet? Well, I think they are wrong. The 1st Q of 2010 saw three straight months of positive employment gains. When was the last time we saw three straight months of positive employment gains? That was in the 4th Q of 2007. I would say the aggregate demand recovery is having a tremendous impact on payroll employment, especially coming off 5 straight negative quarters. If this doesn’t impress the critics, I don’t know what would. In addition, the April gain in payroll employment is the 2nd largest in 10 years.

ReplyDeleteOne reason the unemployment rate increased in April is because more people entered the labor force. This is actually not a bad reason for the unemployment rate to rise because people are now looking for jobs because they must feel the economy is improving. I find economists who worry about productivity gains causing unemployment are lousy economists.

You know TFP is measured as a residual. How can we make policy prescriptions based upon the cocient of a division?

ReplyDeleteThis article made me think of the Dell computer story. First it was one of the greatest stocks ever,its stock price doubling repeatedly. Dell was justly praised for the efficiency of its business model. Later, with the end of the tech boom, Dell's successful business model became a "commodity" model, and its capacity for growth disappeared. The end point of its efficiency model appears to be an arid, no-growth desert, and initiative in its industry has passed to Apple and HP, companies more willing to bear the costs of a consumer business, with retail distribution and branding.

ReplyDeleteI'm no economist or stock market professional, but I wonder if all the forces that have promoted globalization have not taken us to an endpoint of an efficiency trend like that of Dell Computer Co. If so, does economic theory teach us anything about how to move away from what I'm calling the "desert" of efficiency, with its manifest deficiencies in creating full employment, to a more job abundant, if less efficient, full employment economy? How do we get out of the high productivity efficiency box? Decades of trickle down? Some explicit re-distributionist approach?

One more observation based on Dell. It is my understanding that Dell has been a ruthless exploiter of competitive efforts of states, municipalities, and even nations such as Ireland to attract "jobs" by granting tax abatements. Is this race to the bottom by governments a factor in the multiple financial crises faced by governments where liabilities and deficits greatly outweigh revenue streams. Here a form of governmental "efficiency" in leveling the economic playing field by simplifying tax structures and leveling tax burdens across the multiple jurisdictions may be part of the answer.