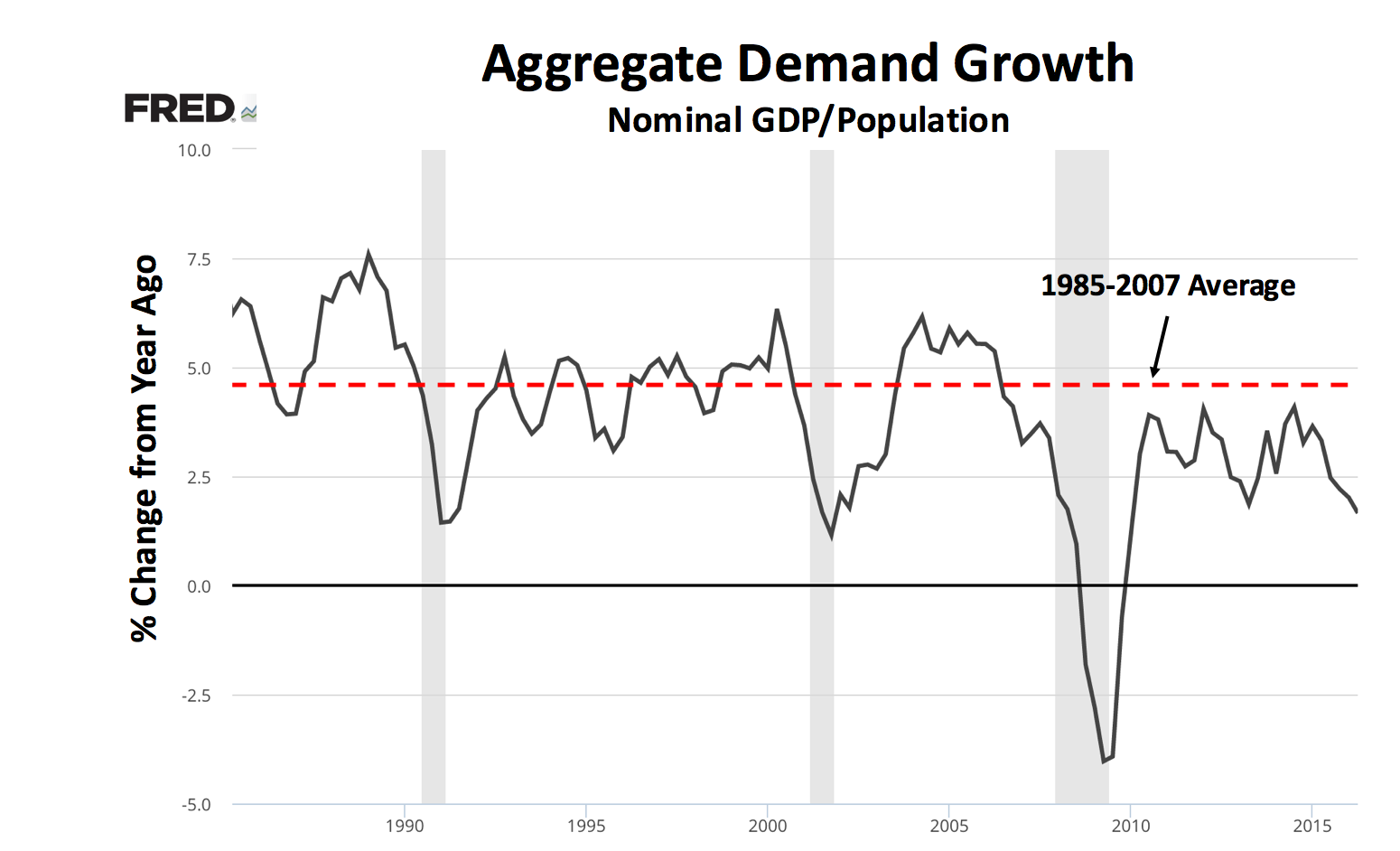

Nominal demand is a shadow of its former self. In the past, it averaged near 5% annual growth but has struggled ever since the crisis. The figures below illustrate this on a per capita basis for aggregate demand and domestic demand growth.

Nominal demand growth ain't what it used to be. To be clear, nominal demand growth is not what we ultimately care about. That would be real economic growth and over the long run it is not determined by nominal demand growth but by real factors.

That, however, is not my point here. My point is that somehow policy makers were able to generate near 5% nominal demand growth per person pre-2008 and now seem completely unable to do so. Why?

My answer is that inflation targeting, as it is currently practiced, has become the poisoned chalice of macroeconomic policy.

Central banks have been so good at creating low inflation since the early 1990s that it is now the expected norm by the body politic. Any deviation from low inflation is simply intolerable. In the US, everyone from the media to politicians to the average person start to freak out if inflation heads north of 2%. This mentality seems even worse in Europe. Inflation-targeting central banks, in other words, have worked themselves into an inflation-targeting straitjacket that has removed the few degrees of freedom they had. It is hard to imagine Yellen and Draghi being able to raise inflation temporarily above 2% in this environment. All they can do is operate in the 1-2% inflation window. Inflation targeting's success has become it own worst enemy.

Another way of saying this is that the space for doing macro policy has shrunk to the small window of 1-2% inflation. Not only is monetary policy constrained by this, but so is fiscal policy...

For these reasons inflation targeting has become the poisoned chalice of macroeconomic policy. It was a much needed nominal anchor in the 1990s that helped restore monetary stability. Its limitations, however, have become very clear over the past decade and now is preventing the world from having the recovery it needs...

Put differently, nominal demand growth has been weak because the Fed's past successes now prevent it and Congress from allowing the economy to temporarily run a little hot. This shortcoming is a big deal.

If a trucker gets stuck in traffic jam, he will have to temporarily speed up afterwards to make up for lost time. On average, his speed for the trip will be the legal speed limit but only if he temporarily speeds up after the traffic jam. Likewise, an economy may need temporarily higher-than-normal inflation after a sharp recession to return to full employment. This also implies temporarily higher-than-normal nominal demand growth. On average, this temporary pickup will keep inflation and nominal demand growth on target. Running a little hot, therefore, is necessary sometimes. Currently, however, this policy flexibility is not possible.

Seven years after the crisis this shortcoming still seems to be a problem. Even if we are closer to full employment, the inflation targeting straightjacket is still keeping nominal demand growth weak. This is unfortunate, especially if potential GDP has been affected by the sustained shortfall in nominal demand growth.

What is needed, then, is a monetary policy rule that anchors long-term price stability but provides for short-run price flexibility. Enter NGDP level targeting. It does all the above and then some.

Some of us have been making this argument for years. So it was nice to see this letter from San Francisco Fed President John Williams yesterday:

[C]entral banks and governments should critically reassess the efficacy of their current approaches and carefully consider redesigning economic policy strategies to better cope with a low r-star environment...

Turning to policies that can help stabilize the economy during a downturn, countercyclical fiscal policy should be our equivalent of a first responder to recessions, working hand-in-hand with monetary policy... One solution to this problem is to design stronger, more predictable, systematic adjustments of fiscal policy that support the economy during recessions and recoveries (Williams 2009, Elmendorf 2011, 2016)...

Finally, monetary policy frameworks should be critically reevaluated to identify potential improvements in the context of a low r-star... inflation targeting could be replaced by a flexible price-level or nominal GDP targeting framework, where the central bank targets a steadily growing level of prices or nominal GDP, rather than the rate...

John Williams is exactly right. NGDP level targeting is a great solution to the nominal demand shortfall and it can be implemented in a way that systematically utilizes both monetary and fiscal policy. This is done by having the Fed adopt a NGDP level target that is backstopped by the U.S. Treasury Department. It would be a rules-based way to use the power of the consolidated balance sheet of the U.S. government. Let's make nominal demand great again!

P.S. Here is the Chuck Norris and Jean-Claude Van Damme version of my NGDPLT proposal.

P.S. Here is the Chuck Norris and Jean-Claude Van Damme version of my NGDPLT proposal.

The fear of market monetarism is that the "market" won't allow the Fed to control the amount of monetary stimulus - vast amounts of monetary stimulus will trigger uncontrollable inflation. Of course, that's the point of market monetarism. Sumner et al. respond by saying that the "market" will be mostly if not entirely dormant, because the Fed will implement monetary policies that are intended to make it dormant (i.e., to achieve the NGDP target). It's a circular argument that causes critics' heads to spin. My view is that markets are much better at predicting the future than soothsayers, I mean economists, so I'd rely on markets.

ReplyDeleteWhat we need is a different way of thinking about this problem.

ReplyDeleteA revolution took place in economics following the 1930s collapse of the 19th century classical/neoclassical paradigm imbedded in free-market ideology. That paradigm was replaced following World War II by what became known as the neoclassical-synthesis guided by a mixed-economy ideology. Collapse of the neoclassical-synthesis in the 1970s led to its integration with the old 19th century paradigm and ideology into a new-neoclassical synthesis that reverted back to the old free-market ideology of the 19th century. In 2008 that synthesis, as with those that came before, proved to be little more than a house of cards resting on a foundation of sand.

It is not at all clear what kind of paradigm will emerge from the chaos within the discipline of economics that has resulted from the dramatic failure of the new-neoclassical synthesis to provide a context within which the Crash of 2008 and its aftermath can be understood or explained, but it is clear that in the absence of a sea change in the thinking of mainstream economists we are unlikely to survive the fallout from this crash with our fundamental economic, political, and social institutions intact: http://www.rweconomics.com/BPA.htm , http://www.rweconomics.com/htm/LPLFLPPS.htm , http://www.rweconomics.com/LTLGAD.htm ,and http://www.rweconomics.com/IVR.htm .

David, How do you figure in the slowing velocities of M2 and MZM? How do you see their slowing velocities dragging on the price level?

ReplyDeleteIf I am going to look at money, I actually prefer to use a broader measure of money like the Divisia M4 measure.. Empirically, it does a better job than narrow measures like M2 in conforming to the standard notions of what monetary shocks do to the economy. Josh Hendrickson and I have a paper that demonstrates this (see IRFs near the end).

DeleteDo you use the velocity of divisia in MV = PY?

DeleteIs this the velocity that you use for divisia?

Deletehttps://fred.stlouisfed.org/graph/fredgraph.png?g=6FJj

If so, it is still declining. How do you see this dragging on the price level?

David, Why did you decide to take the average from 1985? It skews the data quite a lot. 1990-2007 is lower but perhaps a more realistic benchmark. Inflation expectations were still quite high in mid to late 80s.

ReplyDeleteI use 1985-2007 since that is a commonly used benchmark period. It is the 'Great Moderation' period.

DeleteThanks David. This paper suggests the structural break too place in the early 1990s though. https://www.federalreserve.gov/econresdata/feds/2016/files/2016035pap.pdf

DeleteI think the modelling of regime changes is quite important in trying to identify appropriate starting points. Sadly there isn't enough data to run a Markov switching model though.

I think George S has mentioned something about a 5% level being too high. A 5% target I think would drive excess liquidity into financial assets. Back to square 1.

Thomas, I actually am a big fan of Selgin's productivity norm. It would be my ideal form of a NGDPLT. However, we have to start somewhere and I suspect that realistically it would be somewhere between 3-5%.

DeleteRight now the Fed is trying for 2pct inflation and approx 3pct growth.

ReplyDeleteHow would NGDP targeting change what they are doing. Doesn't a 2pct inflation target mean the same thing as 5pct NGDP in practice.

As for how the Fed is supposed to be so precise, no one seems to explain. I suppose it could follow the Friedman rule and let money/banks/lending (whatever is your favorite) expand at a nominal 5pct and hope for the best.

But isn't what the government is doing, fiscally and policywise, have a much greater effect on inflation and growth than anything the Fed can do (except in a liquidity crisis perhaps )