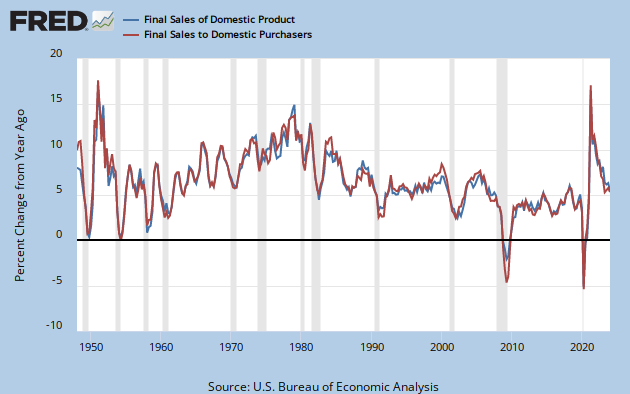

Thanks to Alex Tabarrok, The Economist's Free Exchange blog, Ezra Klein, and Bruce Bartlett my last post on the history of U.S. nominal spending received a lot of attention. It also raised the important question of why we should care about nominal spending. Before I answer this question let me first define nominal spending: it is the current dollar value of total spending in an economy. More simply, it is total demand in an economy. Technically, what I showed in the last post was the growth rate of final sales to domestic purchasers or U.S. domestic demand. One could also look at final sales of domestic product--which includes foreign purchases of U.S. made goods and services--which is aggregate demand for the U.S. economy. Either way, both series show a large collapse in nominal spending late 2008, early 2009 as seen in this figure.

Now on to the importance of nominal spending. I have asserted that the best way for the Fed to reduce macroeconomic volatility is to stabilize nominal spending rather than inflation. Here is why. If an economy is running at full employment, then any sudden increase or decrease in nominal spending will give rise to changes in real economic activity that are not sustainable. This is because there are numerous rigidities that prevent prices from adjusting instantly. There is simply no way to suddenly jar nominal spending (i.e. create a nominal spending shock) and not have real economic activity move as well.

{kind=link}

Now on to the importance of nominal spending. I have asserted that the best way for the Fed to reduce macroeconomic volatility is to stabilize nominal spending rather than inflation. Here is why. If an economy is running at full employment, then any sudden increase or decrease in nominal spending will give rise to changes in real economic activity that are not sustainable. This is because there are numerous rigidities that prevent prices from adjusting instantly. There is simply no way to suddenly jar nominal spending (i.e. create a nominal spending shock) and not have real economic activity move as well.

Note that the key here is not to aim for inflation stability, but to aim for nominal spending stability. This is because inflation is merely a symptom of nominal spending shocks. Moreover, inflation can sometimes can be hard to interpret--Is the high (low) inflation due to positive (negative) aggregate demand (AD) shocks or negative (positive) aggregate supply shocks (AS)?--and as a result monetary policy that targets inflation rather than nominal spending may make the wrong call. To illustrate this point, consider the following two cases*:

(1) A central bank has a 2% inflation target and the economy's sustainable (i.e. natural) rate of growth is 3%. Here we have nominal spending growing at 5%. Now imagine that fiscal policy generates a positive AD shock that increases nominal spending and pushes inflation temporarily to 4%. Now nominal spending is growing at 7% and if there are any nominal rigidities (i.e. upward slopping SRAS curve) this increase in nominal spending (or AD) should also push real economic activity beyond its natural rate. Hence, a positive output gap is created and there is an uptick in inflation. In this scenario--where a positive AD shock is the issue--a policy aiming to stabilize nominal spending would have prevented the output gap from emerging. An inflation target regime would have also addressed the output gap, but since inflation is a symptom of the nominal spending shock it only would have done so after the horse was out of the barn, so to speak. Still, in this case inflation targeting would have made the right call.There are other scenarios one could consider, but any way you slice it what becomes apparent is that monetary policy that targets nominal spending can handle both AD and AS supply shocks, while monetary policy that targets inflation can only handle AD shocks. I believe one example of this was the 2003-2004 period when the U.S. economy was buffeted with rapid productivity gains (i.e. positive AS shocks) that led to low inflation. The Fed interpreted this low inflation as indicating weak AD and kept monetary policy extremely loose. They were wrong, nominal spending was soaring by 2003 and thus, monetary policy was too accommodative. I also believe that had the Fed been targeting nominal spending it would been easier for them to avoid the collapse in nominal spending that occurred in late 2008, early 2009. Of course, an explicit inflation target would have helped too but why not go for root of the problem rather than its symptom?

(2) A central bank has a 2% inflation target and the economy's natural rate of growth is 3%. Once again, nominal spending is growing at 5%. Now assume a permanent productivity innovation pushes the natural rate of real economic growth to 5%. Assume also that the surge in productivity in the absence of any new accommodation or changes in monetary policy--that is, the central bank is still increasing money supply at rate that would have created a 2% inflation target under the old steady state of 3% real growth--would have pushed inflation down to 0%. If the central bank adopts this approach and does not accommodate the increase in productivity, nominal spending will still be at 5% (0% inflation + 5% real growth). Note, there has been no change in AD (still growing at 5%) and thus no movements against the SRAS by which to create an output gap.

Now assume the central doesn't sit idly by but accommodates the productivity shock so that its inflation target is maintained. It will have to stimulate nominal spending such that the potential 2% drop in inflation is avoided. Now nominal spending jumps to 7% from its previous value of 5%. Here, we have a sudden increase in nominal spending (or AD) that in the face of an upward-slopping SRAS will temporarily push output beyond its natural rate. In other words, an positive output gap will emerge. But here there is no observed change in inflation or the inflation target! Had the central bank targeted a 5% nominal spending growth rate this output gap would not have emerged. Instead, its rigid focus on inflation caused it to be too accommodative.

For more on the importance of stabilizing nominal spending I would recommend you take a look at Scott Sumner's blog. Also, here is an article from the St. Louis Fed that provides a more thorough but gentle introduction to the importance of nominal spending and how monetary policy might target it.

* These are variations of scenarios I first posted over at Worthwhile Canadian Initiative.

David:

ReplyDeleteGreat post.

But why not cover the adverse aggreate supply shock, negative aggregate demand shocks too? Certainly those are more relevant today.

Yes, I should have been more thorough and examined all the possible shocks. Out of convenience I just stuck to the two. Your question, though, makes me think there is a need for a paper that provides a thorough discussion of stabilizing nominal expenditures as a policy goal for a general audience. Maybe there is one out there already.

ReplyDelete