About $450 billion or two-thirds of all U.S. currency notes are held outside the United States according to a 2006 U.S. Treasury report. This effectively amounts to an interest-free loan for the United States as it has simply exchanged at some point in the past ink-stained paper for $450 billion worth of goods and services. To boot, the purchasing power of the dollars has eroded making the eventual repayment of these interest-free loans even easier. Of course, if the dollars are never returned to the United States then it is an even better deal for the United States. This is just one of the perks to having the main reserve currency of the world.

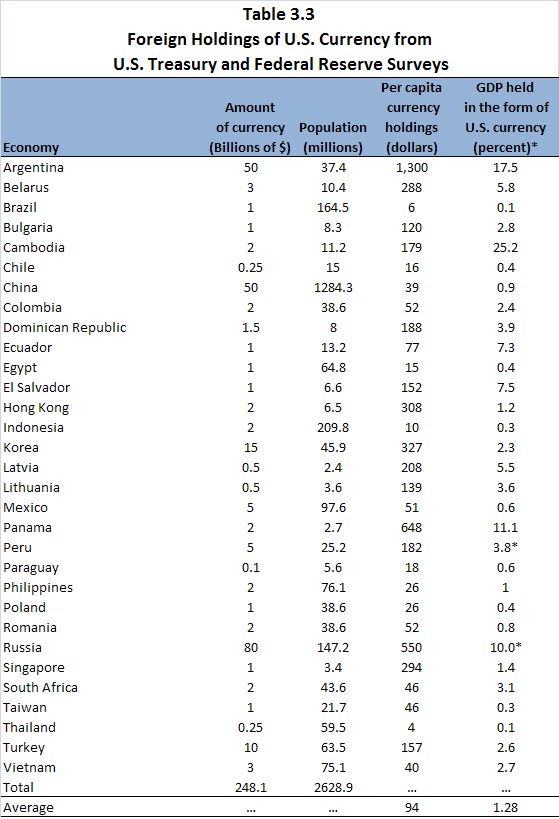

So which countries in the world have been so generous to the United States? Here is a table from the Treasury report that accounts by country for about $250 billion of the total U.S. currency notes held abroad (click on figure to enlarge):

Unsurprisingly, most of the currency is being held by emerging and developing economies. Presumably all of these countries at some point in the past had some form of monetary instability and, as a result, their residents are now demanding a relatively safe alternative form of money, the dollar. So what denominations are these folks holding? Linda Goldberg has put together a nice chart that answers this question:

It is interesting to see the increasing demand for $100 bills and the decreasing demand for $50 and $20 bills. Maybe the dollars are being held more as a store of value than a medium of exchange and, thus, the larger bills are more in demand.

It is interesting to see the increasing demand for $100 bills and the decreasing demand for $50 and $20 bills. Maybe the dollars are being held more as a store of value than a medium of exchange and, thus, the larger bills are more in demand.

So which countries in the world have been so generous to the United States? Here is a table from the Treasury report that accounts by country for about $250 billion of the total U.S. currency notes held abroad (click on figure to enlarge):

Unsurprisingly, most of the currency is being held by emerging and developing economies. Presumably all of these countries at some point in the past had some form of monetary instability and, as a result, their residents are now demanding a relatively safe alternative form of money, the dollar. So what denominations are these folks holding? Linda Goldberg has put together a nice chart that answers this question:

It is interesting to see the increasing demand for $100 bills and the decreasing demand for $50 and $20 bills. Maybe the dollars are being held more as a store of value than a medium of exchange and, thus, the larger bills are more in demand.

It is interesting to see the increasing demand for $100 bills and the decreasing demand for $50 and $20 bills. Maybe the dollars are being held more as a store of value than a medium of exchange and, thus, the larger bills are more in demand.

Nobody claims that the US gets an interest-free loan when foreigners send us goods in exchange for shares of IBM stock. That's because IBM shares are a liability of a US firm. The trouble with this interest-free loan claim is that green paper dollars are a liability of the Federal Reserve.

ReplyDeleteOn a related note, nineteenth-century banks that issued paper dollars generally claimed that the issue of paper dollars was unprofitable, and banks mainly issued them as a form of advertising. It seems the costs of printing, handling, counterfeiting, etc. outweighed the interest earned by the bank. The Fed is not immune to these things.

And maybe the 100s are being used as a medium of exchange for illicit/black market transactions.

ReplyDeleteGood point Anonymous.

ReplyDeleteOne price that the US DOES pay is a smallish debasement of the currency through counterfeiting. Of course, this was the stated reason for the new design, rather uglier to my, any many others', eyes. While new counterfeits must be a much smaller amount than the interest-free loan or even loss/destruction of notes, it's still something worth a bit of effort.

ReplyDeleteI'm surprised that the Treasury/Fed hasn't embedded the notion of a non-repudiatable contract into the serial number as a protection against forgery. If the serial number expanded to a unique 1000-bit pattern on each bill that could be licensed out to banks worldwide, it'd be virtually impossible to concoct numbers; they'd have to duplicate good bills' numbers, which could easily be detected in said "bill validators" connected up to the Fed. (You wouldn't want the key validation logic anywhere outside of Washington.)

Hi- I've heard the claim before that dollars held outside the US amount to an "interest free loan" for the US, but I'm not sure exactly _how_ that would work. HOW does it become a loan?

ReplyDeleteCan someone explain that to me?

Yams, the idea is that the United States traded a piece of paper (dollars) for some real good or service to a foreigner. In turn, the piece of paper entitles the holder to some U.S. good or service. The holder of the dollar, however, only gets the face value amount. Thus, no interest.

ReplyDelete