The Cleveland Fed has launched a new website that will provide on a monthly basis estimates of expected inflation over various horizons. These estimates are supposed to be cleaner than those coming from Treasury inflation-protected securities (TIPS) which are contaminated by risk premia. The model that is the basis for these estimates can also be used to derive real interest rates and an inflation risk premium. This is a great addition to the universe of online economic data and the Cleveland Fed should be commended for providing it to the public.

The numbers for June 2010 are not pretty. Here is the lead paragraph:

The first of these data points says that the market expects inflation to be 1.34% over the next year. A closer look at the data for the whole year indicates this broad decline in inflationary expectations is not a one-time drop. Inflation expectations are down for the first half of this year. These findings confirm the point I have been making with TIPS data: the market expects aggregate demand to slow down over the next year. And the Fed's failure to stabilize these expectations means that monetary policy is effectively tightening.

The first of these data points says that the market expects inflation to be 1.34% over the next year. A closer look at the data for the whole year indicates this broad decline in inflationary expectations is not a one-time drop. Inflation expectations are down for the first half of this year. These findings confirm the point I have been making with TIPS data: the market expects aggregate demand to slow down over the next year. And the Fed's failure to stabilize these expectations means that monetary policy is effectively tightening.

Speaking of tightening, below is the Cleveland Fed's estimates of the 1-month real interest rate that comes from the same model generating the expected inflation series. (The red highlight and related commentary are mine):

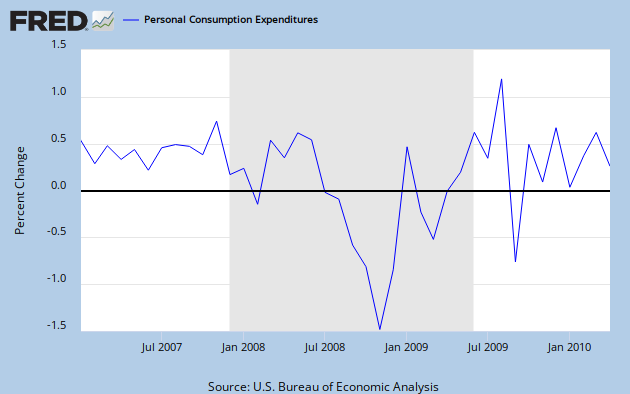

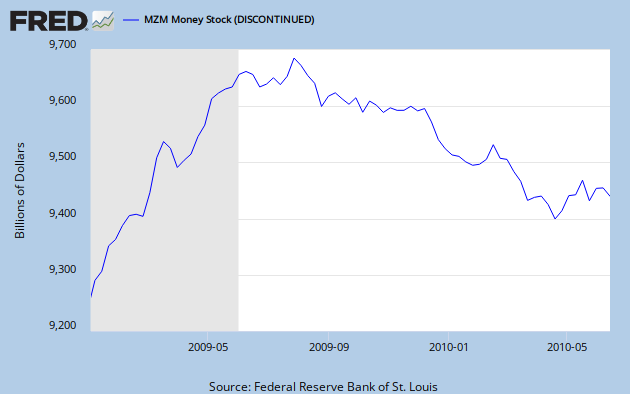

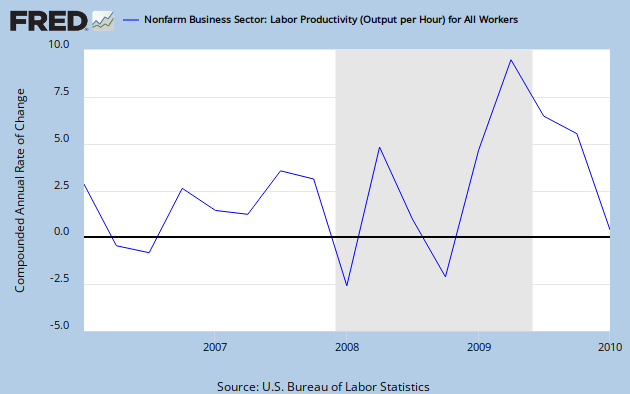

So real interest rates spiked in November 2008 and stayed elevated through March 2009. This bit of evidence lends support to Scott Sumner's claim that monetary policy effectively tightened here and helped usher in the Great Recession.

Go check out the website.

The numbers for June 2010 are not pretty. Here is the lead paragraph:

The Federal Reserve Bank of Cleveland reports that its latest estimate of 10-year expected inflation is 1.84 percent. In other words, the public currently expects the inflation rate to be less than 2 percent on average over the next decade.It gets worse. This 1.84% is down from the previous month as is all yearly horizons of inflation expectations. This can be seen in the following Cleveland Fed figure. This figure shows the expected inflation over maturities ranging from 1 to 30 years:

The first of these data points says that the market expects inflation to be 1.34% over the next year. A closer look at the data for the whole year indicates this broad decline in inflationary expectations is not a one-time drop. Inflation expectations are down for the first half of this year. These findings confirm the point I have been making with TIPS data: the market expects aggregate demand to slow down over the next year. And the Fed's failure to stabilize these expectations means that monetary policy is effectively tightening.

The first of these data points says that the market expects inflation to be 1.34% over the next year. A closer look at the data for the whole year indicates this broad decline in inflationary expectations is not a one-time drop. Inflation expectations are down for the first half of this year. These findings confirm the point I have been making with TIPS data: the market expects aggregate demand to slow down over the next year. And the Fed's failure to stabilize these expectations means that monetary policy is effectively tightening.Speaking of tightening, below is the Cleveland Fed's estimates of the 1-month real interest rate that comes from the same model generating the expected inflation series. (The red highlight and related commentary are mine):

So real interest rates spiked in November 2008 and stayed elevated through March 2009. This bit of evidence lends support to Scott Sumner's claim that monetary policy effectively tightened here and helped usher in the Great Recession.

Go check out the website.

{kind=link}

{kind=link}

{kind=link}