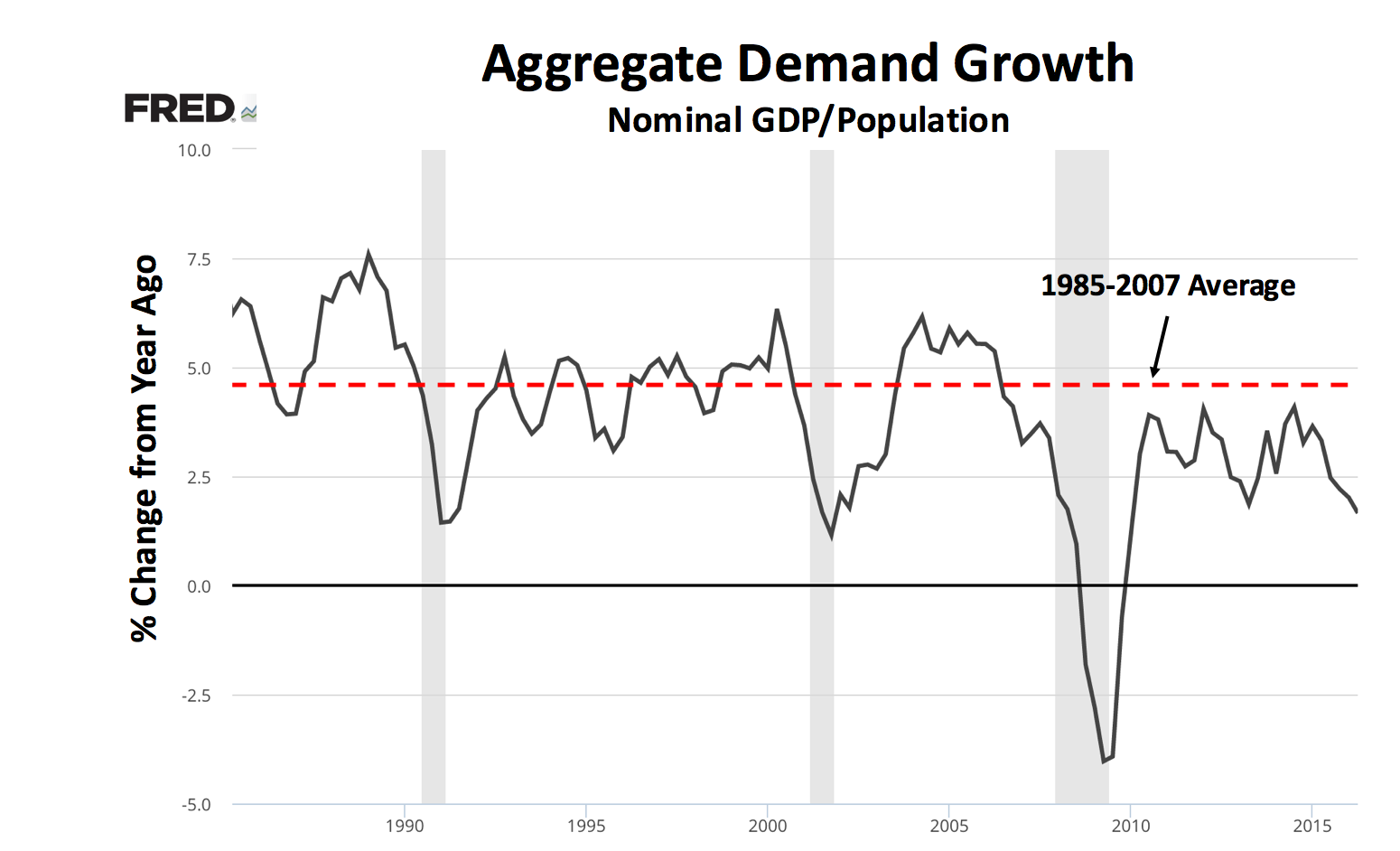

Nominal demand is a shadow of its former self. In the past, it averaged near 5% annual growth but has struggled ever since the crisis. The figures below illustrate this on a per capita basis for aggregate demand and domestic demand growth.

Nominal demand growth ain't what it used to be. To be clear, nominal demand growth is not what we ultimately care about. That would be real economic growth and over the long run it is not determined by nominal demand growth but by real factors.

That, however, is not my point here. My point is that somehow policy makers were able to generate near 5% nominal demand growth per person pre-2008 and now seem completely unable to do so. Why?

Central banks have been so good at creating low inflation since the early 1990s that it is now the expected norm by the body politic. Any deviation from low inflation is simply intolerable. In the US, everyone from the media to politicians to the average person start to freak out if inflation heads north of 2%. This mentality seems even worse in Europe. Inflation-targeting central banks, in other words, have worked themselves into an inflation-targeting straitjacket that has removed the few degrees of freedom they had. It is hard to imagine Yellen and Draghi being able to raise inflation temporarily above 2% in this environment. All they can do is operate in the 1-2% inflation window. Inflation targeting's success has become it own worst enemy.

Another way of saying this is that the space for doing macro policy has shrunk to the small window of 1-2% inflation. Not only is monetary policy constrained by this, but so is fiscal policy...

For these reasons inflation targeting has become the poisoned chalice of macroeconomic policy. It was a much needed nominal anchor in the 1990s that helped restore monetary stability. Its limitations, however, have become very clear over the past decade and now is preventing the world from having the recovery it needs...

Put differently, nominal demand growth has been weak because the Fed's past successes now prevent it and Congress from allowing the economy to temporarily run a little hot. This shortcoming is a big deal.

If a trucker gets stuck in traffic jam, he will have to temporarily speed up afterwards to make up for lost time. On average, his speed for the trip will be the legal speed limit but only if he temporarily speeds up after the traffic jam. Likewise, an economy may need temporarily higher-than-normal inflation after a sharp recession to return to full employment. This also implies temporarily higher-than-normal nominal demand growth. On average, this temporary pickup will keep inflation and nominal demand growth on target. Running a little hot, therefore, is necessary sometimes. Currently, however, this policy flexibility is not possible.

Seven years after the crisis this shortcoming still seems to be a problem. Even if we are closer to full employment, the inflation targeting straightjacket is still keeping nominal demand growth weak. This is unfortunate, especially if potential GDP has been affected by the sustained shortfall in nominal demand growth.

What is needed, then, is a monetary policy rule that anchors long-term price stability but provides for short-run price flexibility. Enter

NGDP level targeting. It does all the above and then some.

[C]entral banks and governments should critically reassess the efficacy of their current approaches and carefully consider redesigning economic policy strategies to better cope with a low r-star environment...

Turning to policies that can help stabilize the economy during a downturn, countercyclical fiscal policy should be our equivalent of a first responder to recessions, working hand-in-hand with monetary policy... One solution to this problem is to design stronger, more predictable, systematic adjustments of fiscal policy that support the economy during recessions and recoveries (Williams 2009, Elmendorf 2011, 2016)...

Finally, monetary policy frameworks should be critically reevaluated to identify potential improvements in the context of a low r-star... inflation targeting could be replaced by a flexible price-level or nominal GDP targeting framework, where the central bank targets a steadily growing level of prices or nominal GDP, rather than the rate...

John Williams is exactly right. NGDP level targeting is a great solution to the nominal demand shortfall and it can be implemented in a way that systematically utilizes both monetary and fiscal policy. This is done by having the Fed adopt a NGDP level target that is

backstopped by the U.S. Treasury Department. It would be a rules-based way to use the power of the consolidated balance sheet of the U.S. government. Let's make nominal demand great again!

P.S. Here is the

Chuck Norris and Jean-Claude Van Damme version of my NGDPLT proposal.

{kind=link}

{kind=link}