Barron's is running an article of mine this week titled "

Deflation Isn't Always Dangerous." I make the case in the article that the failure of the Federal Reserve to distinguish between aggregate demand-driven and aggregate supply-driven deflationary pressures during the 2002-2003 deflation scare was a contributing (not sole) factor to the U.S. housing boom-bust cycle. The Fed read the deflationary pressures of this time as indicating weak aggregate demand; the evidence to me clearly points to rapid productivity gains being the source of the downward price pressure. In turn, this rapid productivity growth implied a higher neutral interest rate, but the Fed pushed its policy rate to historically low levels creating a Wicksellian-type disequilibrium.

For more details on this argument see these other related postings of mine:

here,

here,

here,

here, and

here. If you read the Barron's article and are interested in the Postbellum deflation experience I briefly discussed in it, then check out my article titled "

The Postbellum Deflation and Its Lessons for Today." I address some of the common critiques of this period's deflation in this article and show that this period's deflation was in fact largely benign.

Update

For some reason, the on-line version of my essay has several typos. So in case you do not have access to typo-free print version, here is how the on-line version should read as follows:

Deflation Isn't Always Dangerous

By DAVID BECKWORTH

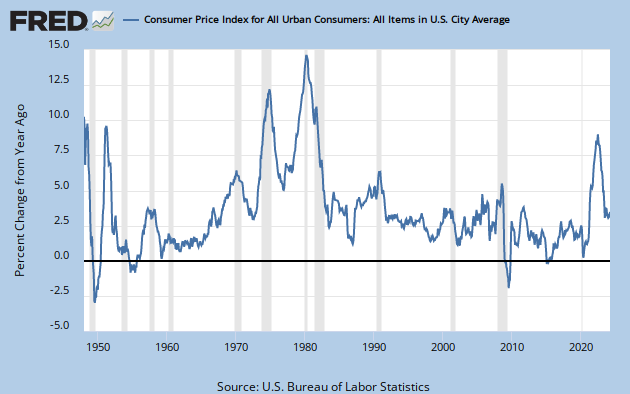

IN 2003, AT THE HEIGHT OF THE deflation scare, Gary Stern was one of the few voices in the Federal Reserve System questioning whether the deflationary pressures of the time were truly a threat to macroeconomic stability. As president of Minneapolis Federal Reserve Bank, he was not convinced that the falling inflation rate was something to be feared. He viewed disinflation as a natural outcome of the economy's productivity gains. In his view, there was no need to cut the federal-funds rate to historically low levels.

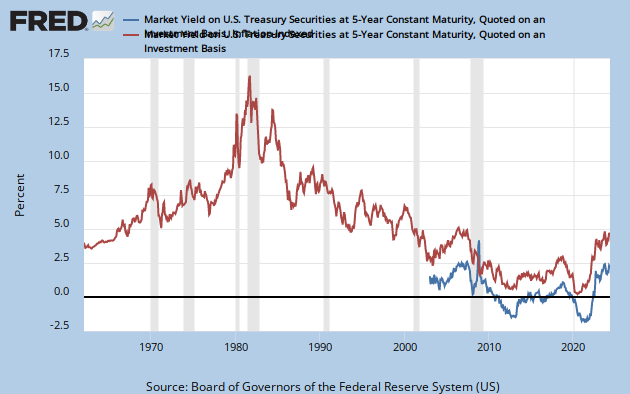

Most officials in the Federal Reserve System, however, viewed the low inflation rate that time with alarm. They worried that it was the consequence of weakening demand in the economy. Their view prevailed and the federal-funds rate was cut to historically low levels. The inflation-adjusted, or real, federal-funds rate was pushed into negative territory and held there until 2005.

This move by the Federal Reserve appears to have been overly accommodative, and is now considered by many to be a key reason for the boom and bust in housing and related imbalances in financial markets.

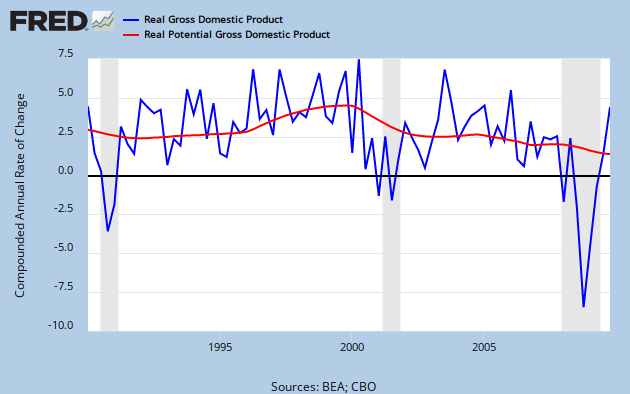

Productivity was growing around 3% a year between 2002 and 2005, a rapid pace by historical standards. But today's conventional wisdom on deflation still is shaped by painful deflation experience of the Great Depression in the 1930s. Those who remember the past are afraid of repeating it.

Deflation -- an actual decline in prices -- can cause economic harm through several channels.

First, given relatively rigid input prices, such as wages, an unexpected deflation will lower firms' profit margins, reducing production and employment.

Second, unexpected deflation means debt becomes more onerous, leading to an increase in delinquencies and defaults, followed by weakening balance sheets of financial institutions and reduced lending.

Third, since actual interest rates reflect a real-interest-rate component and an expected-inflation component, deflation could pull short-term interest rates down to their lower bound of zero and prevent the central bank from being able to provide additional economic stimulus through cuts in interest rates.

Such events could reinforce each other in a deflationary spiral: Expectations of more deflation lead to a further fall in economic activity and push the economy into a prolonged economic slump.

This conventional wisdom, however, assumes deflation is always the result of a weakening in aggregate demand. It fails to consider that deflation may also arise from a boost to aggregate supply that is not accommodated by an easing of monetary policy. This benign form of deflation occurs as the result of productivity advances that lower per-unit costs of production and, in conjunction with competitive forces, put downward pressure on output prices. Here, profit margins are likely to remain stable even if input prices, such as wages, are relatively rigid, since the decline in a firm's sales price will be matched by the decline in its per-unit costs of production. Bank lending should not be adversely affected, either, since any unanticipated increase in the debt burden should be offset by a corresponding unanticipated increase in real income.

Productivity gains, which imply a faster growing economy, also typically imply a higher real interest rate to maintain economic stability, which in turn should prevent the actual interest rate from hitting the lower bound of zero.

Although rare today, this benign form of deflation emerged following the U.S. Civil War and persisted for almost 30 years while the economy experienced rapid economic growth and the U.S. became the leading industrial power of the world. Deflation in its benign form can be consistent with robust economic growth. Most Federal Reserve officials, however, simply failed to consider this possibility during the 2003 deflation scare.

The Fed missed the distinction and made the wrong call. It lowered real interest rates when productivity was growing. Its policy accelerated domestic spending when the economy was already being boosted by a series of positive aggregate supply shocks. The subsequent economic growth, therefore, had both a sustainable component -- the productivity gains -- and an unsustainable component -- the monetary stimulus.

Interestingly, the lowering of real interest rates and the subsequent credit boom all occurred without any alarming increases in the inflation rate -- the standard sign of overheating economy. This apparent stability, however, was illusory, since the inflation rate did indicate overheating relative to mild deflation rate that would have emerged from the productivity gains had there not been such a lax monetary policy in 2003.

The current problems in the U.S. economy are in part a failure of deflation orthodoxy. Federal Reserve officials, following conventional wisdom on deflation, misread the deflationary pressures in 2003 and fueled financial imbalances that today are just beginning to be worked out. Moving forward, it is important that the two forms deflation and their policy implications be better understood by monetary authorities. History can repeat itself, and sooner than we may now think.

Update II

The typos have been fixed in Barron's.

Now, take a look at the scatterplot using 5-year growth rates (without any adjustments):

Now, take a look at the scatterplot using 5-year growth rates (without any adjustments): Again, an output price-asset price trade off is suggested by the figure. To whiten some of the noise in the scatterplot, I once again remove points from quadrant 3. Now the scatterplot looks as follows:

Again, an output price-asset price trade off is suggested by the figure. To whiten some of the noise in the scatterplot, I once again remove points from quadrant 3. Now the scatterplot looks as follows: These figures all indicate there is a potential trade off between stabilizing output prices and asset prices. While further refinements are needed in these figures, they add perspective to what I have been

These figures all indicate there is a potential trade off between stabilizing output prices and asset prices. While further refinements are needed in these figures, they add perspective to what I have been

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}