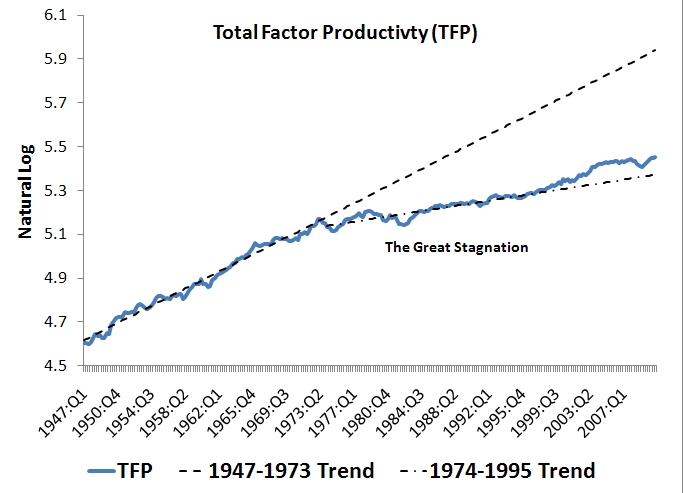

I have been reading with interest the discussion surrounding Tyler Cowen's new book,

The Great Stagnation. The main argument of the book is that the technological progress has slowed. We have picked the "low-hanging fruit" of economic growth and now are mired in slow growth. Count me a skeptic on this one. I believe we have just gone through one of the greatest technological innovations of our time with the advent of the internet and faster computing. Moreover, these technologies are still improving and the potential positive spillover effects from the rest of the world catching up with the advanced economies are tremendous (e.g. imagine what will happen to R&D funding on cancer and AIDS once several billion Asians are rich enough to start demanding it). Rather than a great Stagnation, I see us at that cusp of a Great Acceleration.

Regarding the past few decades, Cowen cites the decline in median income to support his thesis. I can only cite anecdotal evidence, but it is highly convincing to me. The evidence is this: ask yourself how much more productive you are today than you were before the internet and faster computing. In all areas of my life--work, family, travel, enertainment, religion, health, recreation, etc.--I can come up with many examples of where I am now more efficient (or at least have the potential to be more efficient). Some of these gains get reflected in official statistics. Many, however, do not as they are hard to measure. This is not surprising since most of these gains are in the service sector of the economy, a sector where output and productivity have been notoriously hard to measure. For this reason, I believe the data understates the economic gains over the last few decades.

To rectify this measurement problem, I thought I would make an exhaustive list of the all the productivity gains in my life that are the result of the internet and faster computing. But then I realized, one, nobody would want to see them and, two, CTU's

Jack Bauer could do a much better job than I ever could. Yes, the famed counterterrorism agent from the show 24 knows first hand how much more effective he is at getting the terrorists because of these gains. You see, he tried his hand at counterterrorism in 1994 and was not too successful because the technology just was not there. Here is a video clip that documents his problems:

While humorous, this video clip makes it very clear why I find it hard to buy into the Great Stagnation Hypothesis.