Can the Fed really add more stimulus by lowering the interest paid on excess reserves (IOER)? Many observers say yes and are encouraged by the ECB's decision to do just that. The idea behind this belief is that banks would invest their excess reserves in other assets if the IOER was below, or at least equal to, the market interest rate for safe assets. This rebalancing of banks' portfolios would in turn cause a rebalancing of the non-bank public's portofolio and help kickstart a recovery.

The folks at FT Alphaville, however, are not so sure. They see problems with lowering the IOER. They are concerned that doing so would eliminate the net interest margin for money market funds (MMFs) and drive them out of business. The funds sitting at MMFs would then move directly to banks, which also face low net interest margins and increasing FDIC fees. Banks, then, might start charging customers for deposit accounts and this, in turn, might cause the public to want to hold more cash. As a result, financial intermediation would further weaken and the economy would sink even more.

That is a scary story. The folks at FT Alphaville say the only way to avoid this outcome is if fiscal policy complimented the lowering of IOER by providing more safe assets in which financial firms could invest their would-be costly excess reserves. Cardiff Garcia of the FT Alphaville wants to know what the Market Monetarists, long-time advocates of lowering the IOER, think of this scary scenario.

Here is my take. The FT Alphaville story fails because it ignores the broader effect of the Fed lowering the IOER. Such an announcement, if credible, would send a loud signal to markets of more monetary stimulus. And if done right, this signal would have a huge impact because lowering the IOER is tantamount to saying the Fed is going to permanently increase the monetary base. A permanent increase in the monetary base implies a permanently higher price level and permanently higher NGDP level down the road. In other words, lowering the IOER would permanently raise expectations of future nominal spending and income. As a result, demand for financial intermediation services would increase today as firms, households, and governments planned for the higher level of NGDP. The increased demand for credit would raise financial firms' net interest margins and more privately-produced safe assets would appear. No doomsday for MMF and a recovery ensues.

Now I do think that the signal from lowering the IOER would be even more effective if it were done in conjunction with the announcement of a NGDP level target. It would provide a destination point for nominal spending and nominal income that would better focus the public's expectations.

The folks at FT Alphaville are correct, tough, that fiscal policy could be a part of the NGDP recovery process if it created more safe assets. Treasuries and GSEs function as money for many institutional investors and thus are an important part of the money supply and any NGDP recovery. However, the amount of safe assets needed for a full recovery of aggregate demand seems far too large to be met by publicly-created safe assets alone.

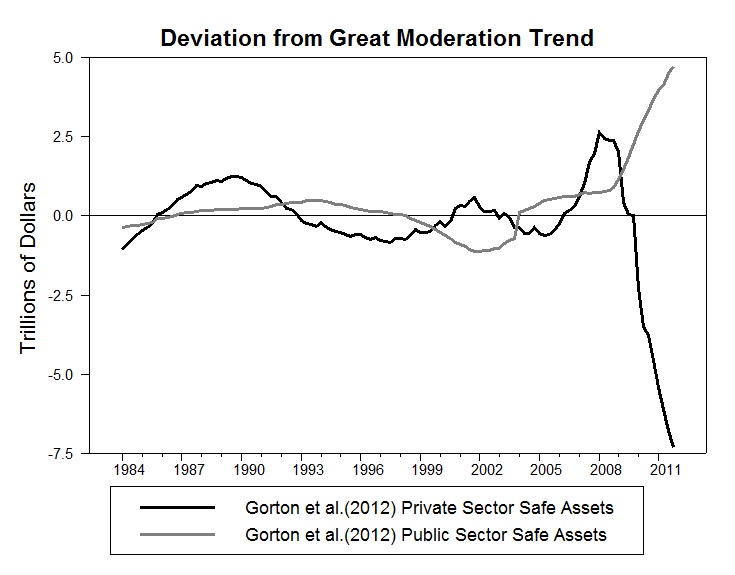

The figures below illustrate this point. The first one shows the total stock of safe assets broken down into privately-produced safe assets and publicly-produced safe assets. (The safe asset series is constructed according to Gorton et al. (2012) and the figures come from a paper on transaction assets I coauthored with Josh Hendrickson.) Note that most safe assets are privately produced.

Privately-produced safe assets have fallen since 2008 and have yet to return to their peak value, let alone their pre-crisis trend. Publicly-produced safe assets have somewhat compensated for the collapse, but not enough. This is self evident from the ongoing slump in nominal spending, but also can be seen in the figure below which shows the deviation of the two series from their Great Moderation (1983-2007) trend in dollar terms.

Publicly-produced safe assets as of 2011:Q4 are approximately $4.7 trillion above trend while privately-produced safe assets are about $7.3 trillion below trend. To fully make up for the collapse of private safe assets, the public sector would have to create another $2.6 trillion in debt. That is not going to happen in this political climate.

But then it is not needed. As outlined above, lowering the IOER and adopting a NGDP level target should incentivize the private production of safe assets and spark a robust recovery in aggregate demand. Lowering the IOER need not be scary.

P.S. I first raised concerns about the IOER back in October, 2008.

P.P.S. Here is a similar comment for Izabella Kaminska at FT Alphaville.

Update: David Glasner also weighs in on lowering the IOER.

P.P.S. Here is a similar comment for Izabella Kaminska at FT Alphaville.

Update: David Glasner also weighs in on lowering the IOER.

When commercial banks make additional loans, their aggregate reserves don't decrease or disappear. So I don't see how lowering the rate of IOR makes all that much of a difference. In the aggregate, they will earn the interest whether they are making loans or not.

ReplyDeleteIOR is monetary stimulus - it is free money provided directly by the central bank to commercial banks that builds up the asset side of their balance sheets. If banks were not carrying so much extra reserves, then offering positive IOR should help stimulate lending, since the policy is in effect a kind of rebate of part of the cost of interbank or discount borrowing of additional reserves. As it is, the policy doesn't matter much since there are already so many excess reserves in the system.

IOR just another interest rate management tool. It helps establish a floor to the policy rate.

Great post David. The Fed cutting IOR and inching toward a ngdplt and Draghi getting in touch with his inner Chuck Norris and it could be off to the races. Stocks seem to be anticipating a positive turn....

ReplyDeleteInteresting post. A couple concrns:

ReplyDelete1. While in principal, it would seem that a lower IOR would create an incentive for banks to seek yield elsewhere, I'm not sure that will actually stimulate more lending given the scarcity of adequate collateral, particularly in real estate. Banks are having enough trouble now putting money to work with too many dollars chasing prime collateral and ignoring the rest and not to mention limitations on the ability of owners to refi given existing debts. So the concern is that the reduction in IOR will not have the intended effect, and may actually squeeze margins further, especially if we continue to see the long term rates move lower. Notwithstanding the above concern, I can at least see the reduced IOR causing lender's to loosen lending standards a bit.

2) In a related point, without looking at the numbers in detail, I would imagine that a large reason for the drop off private safe assets from way above trend to way below trend is due to the fact that the securitization model by which those private safe assets were created no longer functions as well for a variety of reasons. As noted above, at least with respect to real estate, for example, there is a shortage of the type of assets that translate into a CMBS issuance. Point being, I'm not so sure that the mechanisms required for a massive rebound of private safe assets are in place, or at least would be without disruption.

Like the FDIC's unlimited guarantee on non-interest bearing transaction accounts, IOeR's (remunerated excess reserve balances) induce DIS-INTERMEDIATION (where the size of the shadow banking system shrinks, but the size of the commercial banking system remains the same).

ReplyDeleteone thing i noticed from today's ft post is that it seems a large part of their analysis depends on the treasury's inability to auction Bills at negative yields (which the treasury has been advised to allow).

ReplyDeleteI honestly doubt it would have much impact without a corresponding target for the nominal economy... but for that open-ended QE would serve much better.

tempest in a teapot!

Dan Kervick, yes the IOR does provide for improved management of interest rate tageting. But when the floor of this corridor system is above the market rate for safe assets something is wrong.

ReplyDeleteHerm, my point is that if there is a big enough monetary policy shock banks and other investors (including those who park their funds at MMFs and banks) will look elsewhere. Mario Draghi's speech last week was an mild example of this. Now think many magnitudes bigger, like a NGDP target and IOER announcement.

ReplyDeleteAnd even if some MMFs do collapse in the process--which I really can't see happening with the now implicit Fed backup--that is a manageable loss if the economy recovers.

dwb, why don't you write a post on it? I would be glad to publish it here.

ReplyDeleteMy first response to the FT reply today is that they still aren't thinking big enough and are too worried about MMFs. As I mentioned to Herm above, think Mario Draghi's comments last week many magnitudes greater. It seems the FT folks instead are thinking along the incremental QE effect scale.

thanks for the sentiment. I doubt i could say anything that you have not already said a dozen-dozen-dozen. times. repeat as necessary! it seems to be sinking in...

ReplyDeleteMy comment rambles on a bit, so I posted it here: http://carrollfinance.blogspot.com/2012/08/a-practioners-perspective-on.html

ReplyDelete[I had trouble posting the comment, so if this is a duplicate, I apologize]

Thanks Dan. I will link to it.

ReplyDeleteDan, could I repost your piece here?

ReplyDelete