Amidst all the chatter about deflation, Daniel Gross over at Newsweek reminds us that deflation can emerge for two very different reasons: (1) a collapse in aggregate demand or (2) a surge in aggregate supply. This distinction is an important one that is often overlooked when it comes to conduct of monetary policy. Before getting into the policy implications, though, let's look at how these two forms of deflation are different. Here is how Gross describes deflation coming from a collapse in aggregate demand:

The second type of deflation is the result of positive aggregate supply shocks. Here is how Gross explains this form:

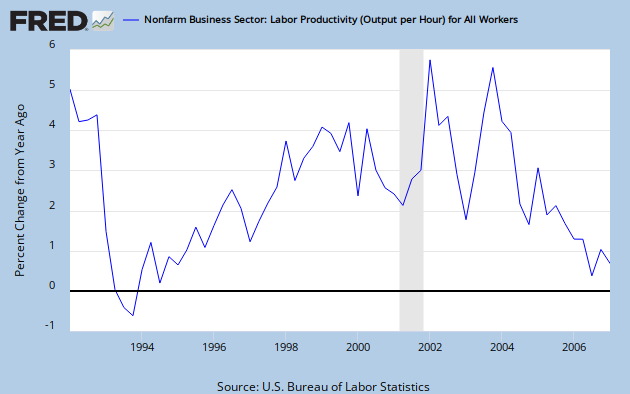

I bring these differences up because it seems clear to me that one of key reason we are this mess now is that the Fed in the early-to-mid 2000s failed to make this distinction. It saw the deflationary pressures of that time as indicating the harmful, demand-induced form when in fact they were the result of the rapid productivity gains at that time. Here is one graph the makes my point:

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

Now in real time it may be hard to distinguish between aggregate demand-induced deflation and aggregate supply-induced deflation. For example, since the U.S. economy had just come out of the 2001 recession it is understandable why the Fed misread the deflationary tea leaves over 2002-2003. Fortunately, there is a way that makes it possible for monetary authorities to avoid making such mistakes: target aggregate demand or some measure of total spending. Stabilize this and the deflation distinction becomes a moot issue.

Read here for more on this issue.

Bad deflation is the kind we had in the Great Depression. "The last time we really had significant deflation in the U.S. was in the 1930s," notes Michael Bordo, professor of economics at Rutgers University. "Between 1929 and 1933, prices fell on average by 15 percent." This deflation was driven by a decline in output, demand, and credit—too little money and wages chasing too many goods and workers. The Depression-era cratering of wages and prices was disastrous because it rendered companies and consumers less able to pay their debts.There is no question this is type of deflationary pressures we experienced during the first half of 2009 and now face again in late 2010. The key to preventing such deflation is to stabilize aggregate demand via monetary policy. Lately, it appears the Fed has been failing to do just this.

{kind=link}

The second type of deflation is the result of positive aggregate supply shocks. Here is how Gross explains this form:

But there have been periods of good deflation, in which prices fell even as the economy boomed. In the 1920s, known to this day as the roaring '20s because of the decade's economic vibrancy, prices fell about 1 percent per year. Between 1870 and 1896, prices fell consistently amid rapid economic growth—with plenty of booms and busts along the way. The reason: innovations like the railroad, the telegraph, electricity, and the assembly line helped farmers, entrepreneurs, and manufacturers to produce and ship their goods more cheaply and efficiently.As mentioned above, the distinction between these two forms of deflation is important when it comes to policy implications. The harmful form of deflation requires aggressive monetary easing to stabilize aggregate demand while the benign form does not. In fact, the benign form of deflation if driven by rapid productivity growth would imply, cetersis paribus, a higher neutral interest rate. Lowering the policy interest rate here would push market interest rates below the neutral rate, lead to excessive monetary easing, and too much current dollar spending. So no need for monetary or aggregate demand stimulus here. In short, both forms of deflation call for stabilizing aggregate demand.

I bring these differences up because it seems clear to me that one of key reason we are this mess now is that the Fed in the early-to-mid 2000s failed to make this distinction. It saw the deflationary pressures of that time as indicating the harmful, demand-induced form when in fact they were the result of the rapid productivity gains at that time. Here is one graph the makes my point:

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.)

This figure shows that the growth rate of domestic demand started accelerating in mid-2002 and continued increasing through late 2004. There were no signs of collapsing demand here. Yet the Fed still saw a threat of demand-induced deflation at least through late 2003. As a result, the Fed continued to push the federal funds rate lower and held it low until mid-2004. What the Fed ignored was that the productivity gains at the time were pushing down the inflation rate. The rest is history. (The Fed also got hung up on the negative output gap. But like the deflationary pressures, much of this gap was being driven the rapid productivity gains not a collapse in demand.){kind=link}

Now in real time it may be hard to distinguish between aggregate demand-induced deflation and aggregate supply-induced deflation. For example, since the U.S. economy had just come out of the 2001 recession it is understandable why the Fed misread the deflationary tea leaves over 2002-2003. Fortunately, there is a way that makes it possible for monetary authorities to avoid making such mistakes: target aggregate demand or some measure of total spending. Stabilize this and the deflation distinction becomes a moot issue.

Read here for more on this issue.

No matter what Krugman writes there are always some who strongly disagree!

ReplyDeletehttp://newmonetarism.blogspot.com/2010/07/deflation.html

Thanks Joao for the link. I posted a comment there.

ReplyDeleteThe best thing out there explaining the different types of deflation is George Selgin's _Less Than Zero_.

ReplyDeletehttp://www.iea.org.uk/files/upld-book98pdf?.pdf

Note well.

The most important causal element is changes in the structure of production and relative prices leading to greater output and value or contractions of output and value.

Only if more output and value are promised will people extend the production process through time.

I.e. longer production processes produce greater output / value hence, longer production processes produce "good deflation".

Similarly, crashes in investment lead to the contraction of the time extent of production, e.g. the crash in the value of the long term capital goods called "houses", crashes in value lead to "bad deflation", the collapse of "shadow money".

I'm guessing economists don't understand any of this, because it applies the logic of marginal valuation to alternative production processes taking different time lengths (a part of the logic of valuation economists have boycotted for 5 generations).

And because macroeconomists don't think like economists (i.e. they really don't to microeconomics, relative prices, and marginal valuation analysis involving multiple production processes and credit and money and multiple "agents".)

If I'm mistaken, provide me with a specific counterexample.

Maybe I'm missing it, if an economy suddenly starts seeing deflation because of an unexpected surge of productivity the correct policy still seems to be monetary easing. Money is used for transactions, more productivity means more transactions can be done so make more money.

ReplyDeleteThe only difference between the two cases is that in the case of productivity the economy enjoys greater growth as it avoids deflation while the economy with collapsing demand simply achieves stability.

ECB: Yes, the financial system is shot and there is a limit to what nominal GDP targeting can do. But, it at least would put us in a more comfortable place to make those changes. Then again, too much comformt might lead to complacency.

ReplyDeleteBoonton: See my linked article above, but in a nutshell adding monetary stimulus after a productivity shock is likely to push the economy too fast.

Without actually having to read the article can you explain why?

ReplyDeleteEven if its easy to overshoot the correct policy is still one of easing, only a tiny bit of easing. Positive productivity shocks, though, are very very rarely dramatically large. The economy grows a small amount every year in productivity as our innovations and know-how make modest improvements (even giant discoveries don't result in instant productivity as it often takes a long time to fully implement them). You're back to Milton Friedman who argued for a constant increase in the money supply to mirror the economy's overall growth rate.

Boonton:

ReplyDeleteLet's say there is an economy-wide positive productivity shock, say due to new technology. Such a shock would push down per unit costs of production for all firms. Now if these firms operate in a competitive environment they will have an incentive to lower their sale price to gain market share. (Note that doing so will not lower their profit margins since per unit costs have fallen too) As a consequence, output prices and thus the price level fall. The economy experiences benign deflation.

Now assume that the central bank attempts to prevent the benign deflation. It eases monetary policy to keep output prices from falling. If successful and if input prices (e.g. wages) are slow to adjust, it will lead to temporarily swollen profit margins. Those swollen profit margins signal more production and the firms respond. The Economy has a boom.

The problem is that the swollen profit margins are only temporary as eventually wages and input costs will adjust. As this happens the profitability of additional production declines and so firms cut back. The economy experiences a bust. So in short, by stabilizing the price level in the advent of a productivity boom, the central bank can create a boom-bust cycle.

I disagree that the deflation would be harmless. Probably less harmful than the deflation we are seeing now but not harmless.

ReplyDeleteLet's say a positive productivity shock lowered the costs of inputs to all goods. All things being equal the economy should expand its production and consumption of goods since it is now cheaper to produce them.

Additional goods means additional transactions and the inputs to a transaction are the good itself and money. More goods requires more money.

In your hypothetical one type of input (wages) are slow to adjust. So as production increases business is able to reap ecnomic profits due to the fact that wages do not rise as much as they should initially. This, though, would seem to be an issue regardless of the money supply. Also to make a big difference one has to havea product that has a very elastic demand curve, otherwise the lower price for it today will only result in a modest increase in demand leaving less justification for rapid expansion of capacity.

This, IMO, is a stretched hypothetical because innovations aren't just implemented instantly. Even very notable inventions like the light bulb, the personal computer, email, spreadsheets etc. were pushed out into the economy rather slowly. The long term productivity gains in the economy are small each year and relatively constant IMO (measured of productivity, though, can be erratic as firms will find productivity increasing in periods of downsizing as the least productive workers are laid off first and decreasing in booms as firms snatch up workers as quickly as they can find them.)

Boonton,

ReplyDeleteYou said: "Additional goods means additional transactions and the inputs to a transaction are the good itself and money. More goods requires more money."

More goods do not require more money if prices are falling. The same amount of money can cover more transactions here.

The hypothetical I sketched is identical to a scenario where an economy starts at full employment and the Fed through monetary easing causes the AD curve to shift right, and given an SRAS, causes output to increase beyond full employment. The only difference is that in my scenario the LRAS curve has shifted out creating a new full employment equilibria and the AD curve shift starts from there. I am not sure this will help, but here and here are some graphs on this topic I sketched from a similar discussion I had with Nick Rowe on this topic.

There is more to this view than just swollen profit margins. As mentioned above, there is also the issue of causing the actual interest rate to deviate from its natural rate. Also, there is the issue of relative price distortions. For a thorough treatment on all these issues--better than you will get here--see this work here by George Selgin. Also, see this piece

by William White.

Consider an economy with a fixed monetary system that experiences a positive productivity shock. Since prices are expected to fall in the future money is not neutral. Just as your 'over compensating' causes overinvestment, this create underinvestment.

ReplyDeleteSince prices are going to fall tomorrow, it makes sense to withhold spending today. Likewise investment purchases make sense to be undertaken tomorrow. A slowdown in overall spending reduces current corporate profits which further lowers incentives towards investment.

In short the inability of the monetary system to accomodate a productivity increase does not appear neutral anymore than overcompensating for a productivity increase is nonneutral.

Boonton:

ReplyDeleteBetween 1866-1897 there was on average deflation of 2% and real economic growth of 4%. No evidence here of a sustained pull back in spending. This period's deflation experience was largely benign and is documented here among other places. This experience and others like it show that there is more to current spending decisions than just the expected price level path. The scenario you describes makes sense in an environment where the real economy is contracting due to negative demand shocks and where there is great uncertainty. This is different, however, from deflation created by positive productivity shocks.

With my argument there is symmetry: if there is a negative productivity shock then should be inflation. In both case the best response by the Fed is to stabilize AD--whether it is a growth target or a level target--and not respond to the productivity shocks. In general, monetary policy can respond effectively to demand shocks but not supply shocks like productivity. I did a post on this latter point here.

Again, I encourage you to look at some of those links above as they address all the question you raise in greater detail.